Substack Library

GlossaryBank Woes + Inflation = Pain

March 17, 2023Happy Friday.

The odds of a hard landing have gone up. A hard landing means rising unemployment and falling stock prices. I want to briefly explain why.

To be clear, no one knows the whole picture. The Fed and the Treasury and the heads of banks and me and you all have questions. What happens in a situation like this, very similar to the pandemic, is that people begin to scramble for information. I’m sure this weekend a lot of people will be banging through spreadsheets, doing the math.

Banking crises happen repeatedly for reasons I’ve shared before:

a) banks are levered.

b) we’ve never figured out how much money to create.

c) we’ve never figured out how tightly to regulate commerce.

The question is how big this crisis is. It’s not yet clear.

Going into this year, I thought we were in the tail end of a tightening cycle and would get what is referred to as a soft landing. Growth would slow, inflation moderate and as the Fed eased up, stock and bond prices would rise. I was long assets and January was great. A soft landing was good news for a long-only investor and good news for a writer (like me) who doesn’t want to follow the market every day!

Last week, SVB bank failed. That got my attention. I had not expected banks to fail. And they failed doing something so dumb it was reasonable to wonder who else was up to the same game.

Last weekend, the Fed and FDIC (Federal Deposit Insurance Corporation) guaranteed all depositor’s funds at the failed banks; equity holders were wiped out. Thursday stocks soared because of a private capital injection into First Republic bank…as I write First Republic stock is off 33%. So the capital injection didn’t work.

Now it is increasingly clear that we have a lingering, post-pandemic inflation issue AND a bubbling, size yet not completely known, banking crisis. It is the banking crisis that is new information that we all need to process.

Here is a framework and facts to help steer you in the right direction, though more facts need to be collected.

Framework: Spending = income plus borrowing.

By this, I mean overall economic activity boils down to you, and you have two sources of spending, what you earn or what you borrow. Income is relatively OK because unemployment is low. Most people have jobs…for now. However, less borrowing = less growth and an abrupt change in borrowing can lead to a recession. Borrowing equals cars, houses, commercial real estate, and business capital investments.

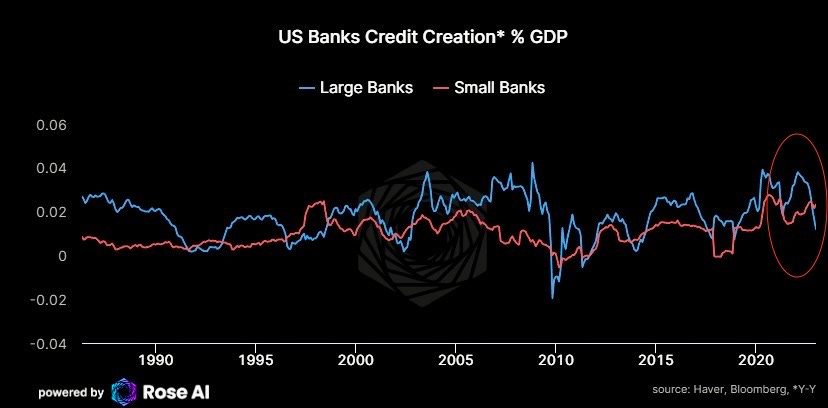

Fact: Smaller banks, the ones that are now having problems, were lending more money than big banks, as the chart below from the smart folks at Rose AI shows. Look at the red circle at the end. It may look like a wiggle, but it matters.

The lines show that the big banks started pulling back their lending a long time ago. Surveys (shown below) showed a tight pull-back in lending but I certainly wasn’t paying attention to who was actually providing the credit. The small banks were doing more.