Substack Library

GlossaryHatch Battening

October 7, 2023Note to readers: know an experienced analyst interested in this type of work? Send me their name.

I am battening down the hatches. And not just because of the shocking news out of Israel. What is catching my attention is a combination of geopolitical and financial stress that is self-reinforcing and dangerous.

The image I have before me is a wave coming that is large and may swamp the boat. By the boat, I mean the rule of law, civilized versus uncivilized, and, more narrowly, asset values. When I get this jittery, I try to remind myself that the instinct has been more reliable than unreliable, but it is not of course 100%. So don’t take the below as advice. You get a window into my thinking, for you to take or leave.

Over the summer, that jittery sense is what led me to warn about US, Japanese, and European bond yields rising. It is also what led me to warn early in 2022 that both stocks and bonds were going to fall and in early 2023, that we would get an asset rally. The underlined sections go to links with the actual post.

I don’t have a crystal ball. I’ve often taken too little risk when I had a hunch something was going to happen and sometimes held on to a position for too long. It’s not only me who makes a hash out of it. All my investment heroes (Soros, Buffett, etc) have too. The key is to get more right than wrong and tolerate the pain along the way. I still have a lot to learn.

Here is the wave that is building and may come crashing down. First the geopolitical, then the financial. Recognize that finance and geopolitical are interconnected. Money wins the war, and so does technology. And those require stable financial conditions to persist, even if the stability of bond yields and civilians getting slaughtered might seem disconnected.

-

In terms of geopolitics, Russia, China, and Iran feel the US and Europe are weak. Whoever planned the Palestinian attack (Iranian financed?) likely thought the same of Israel, also in a political crisis. Putin would not have attacked Ukraine if he didn’t think the Western response would be weak and while he was wrong initially, recent dysfunction in the US Congress must make him elated. Ditto China building out islands to host military bases. The Palestinian attack seems like a suicide mission, but Putin could win in Ukraine, and, if he does, the risks for Taiwan, the Baltics, and other areas rise exponentially. Russia has been trying to control the Bosphorus for 300 years. While US defense spending is multiples higher in dollar terms than Russia and China, the chaos in Congress is a green light for aggressors. These threats then create pressure on defense budgets and national budgets which relates to investment implications (more later on that).

-

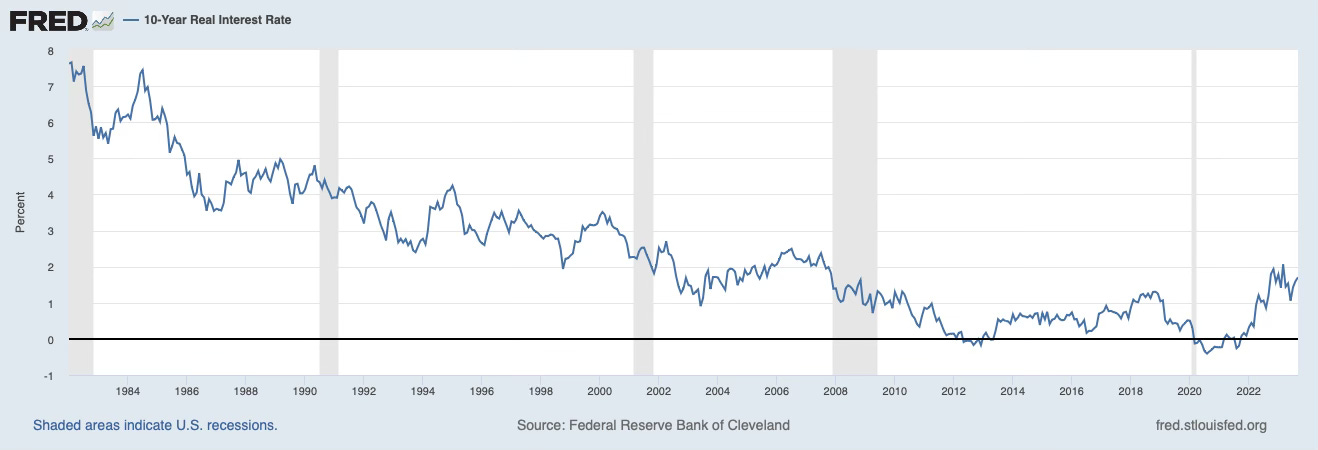

In terms of financing, the thing that has changed is the cost of debt is exploding. Real interest rates, which is the cost of capital after inflation, are the critical rate to watch and have risen a lot. Below is a chart of the US 5-year real interest rate going from negative 1% to over 2% in a short period of time.

To put this in perspective, relative to history this is a 3 standard deviation move, meaning well out of the ordinary. Below is a longer-term history (lacking this month’s moves) of 10-year real interest rates. So while real interest rates are high, and above potential growth, they could go yet higher, strangling the economy. The current US budget deficit is around -6% and will likely blow out to -10% in a recession, though private sector borrowing is drying up and Federal borrowing is only 1/3 of the total.

The interest rate on bonds ties to the cash flows a company can generate. The average profit margin of a US company is around 9%. As the bond yields go up, about 5% for a 10-year government bond, private sector borrowers pay an additional spread. Right about now, the borrowing costs begin to exceed the cash flows, depending on the company. That’s when things could snap.

-

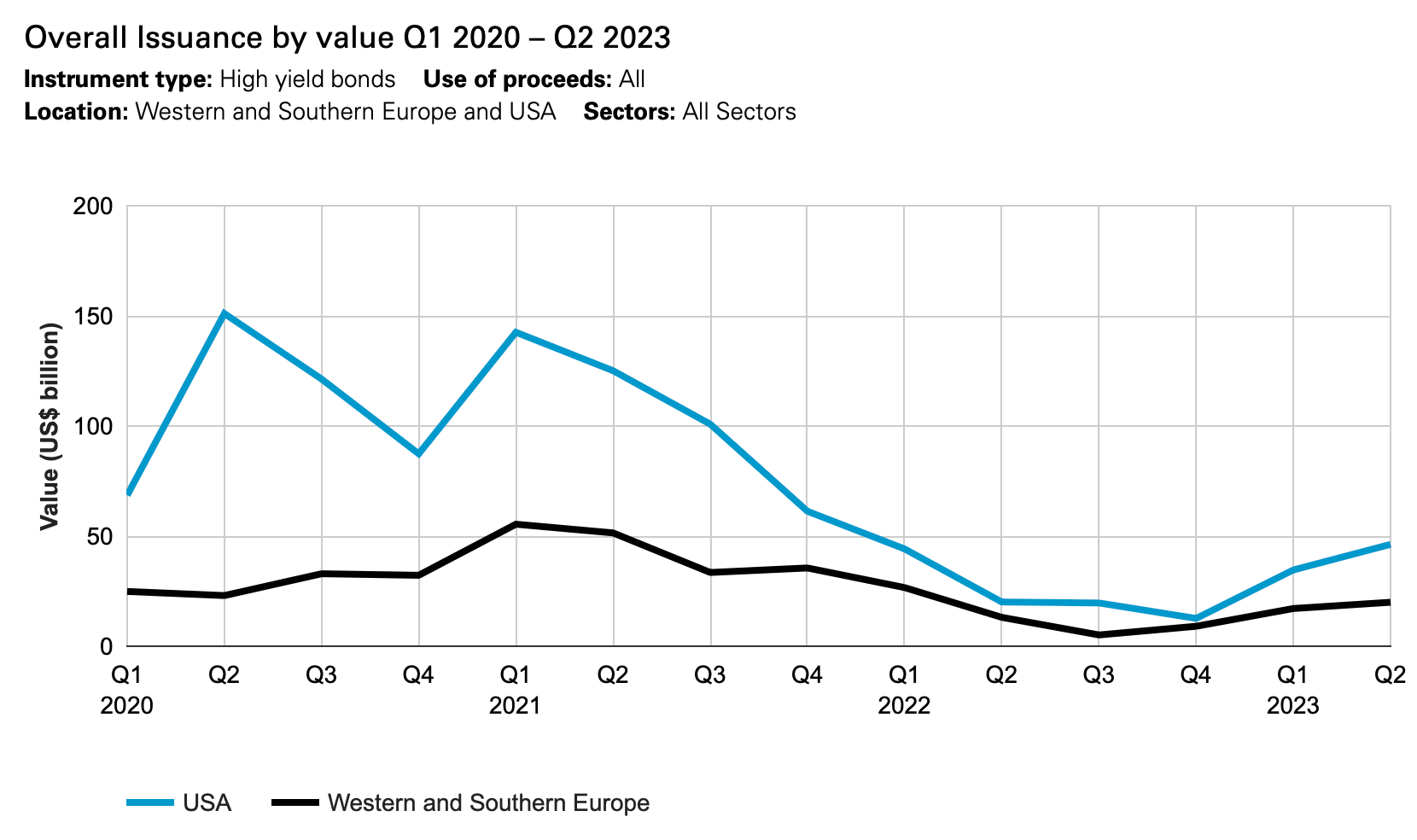

Below is a chart of issuance of high-yield debt in the US and Europe over the last few quarters, tens of billions of dollars of this debt have been issued.

The spread on the high-yield debt is around 400 bps…meaning the total cost is around 9%. I’d have to dig into each individual company to know how sustainable this is, but the big thing is the higher the interest rates go, the more borrowers are cut off. At moments of distress, these spreads can rise much, much higher.

-

Structurally, the US economy, like most major economies, is highly leveraged. The US economy is about $25T and it supports almost $100T of debt. Don’t just stare at government debt to GDP, look at TOTAL debt to GDP. Debt = spending. So if you cut off the debt growth, you cut off spending growth. Then, as spending contracts, debt relative to GDP will initially get worse, because GDP is shrinking. So a country can get into a death spiral when soaring interest rate costs require more issuance, that investors don’t want to pay, so you then need to cut back. This makes it harder to pay for defense. This is the wave I see hitting us. It may take a while. When real interest rates jumped this high in 2006, it took time for problems to manifest, like a year.

-

There are other, more positive scenarios. It’s possible that inflation falls fast and the Fed adroitly responds, which would help the stock market, avoid a recession, and lead to more tax receipts to pay down the debt. That’s just not my central case.

-

The change in interest rates directly feeds into the pricing of stocks.