Substack Library

GlossaryMy Bets

October 10, 2021“I never had a long-term plan. I plan six months ahead. A series of six months plans is a long-term plan.”

It was the early 2000s. I was trying to leave the lumbering commercial bank where I worked. An entrepreneur friend was describing his thinking to me. The same applies to managing money. I try to see through the fog, probabilistically, six months out.

This post is the fourth and final in a series answering a subscriber’s question: what is the bottom line, what are your bets? First I provided a framework for such decisions, then an investment outlook, then a tutorial about how different assets work. Today’s piece is the most technical. Hopefully, all four of the pieces fit together as one.

The “lull” I’ve referred to throughout is a period of time where risky assets like stocks and commodities do well before we face a shift that may be terrible for assets. A rapid Fed tightening and what I’ve called the cult of personality in both the US and China are real risks.

A caveat: THE BELOW IS NOT INVESTMENT ADVICE. INVESTMENT IS RISKY, YOU CAN AND WILL LOSE MONEY. I find people talk about money the way they talk about sex, in private, and suspect we’d probably do better to talk more openly about our investments, compare notes and learn.

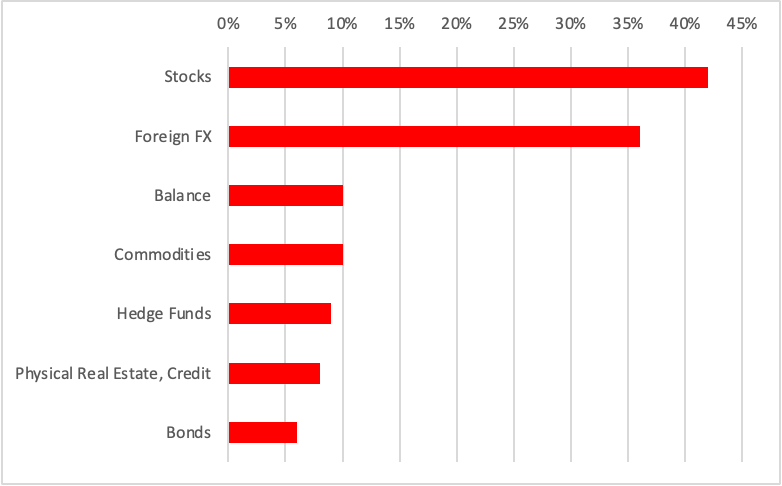

Below is my current portfolio. The numbers are as a percent of capital. If I had $100 in my portfolio, $42 is long stocks.

Here is my thinking:

-

My goal is to earn a 5% to 10% return each year with roughly 10% risk. Managing a portfolio is a trade-off between risk and return. There is a mathematical relationship between these two numbers, confidence in each investment and the ability of certain investments to reduce risk. (This math is what investment pros describe as an “information ratio,” the expected return divided by the expected risk.) Suffice to say, you need to know your own goals and risk tolerance and think about what can hurt you.

-

My starting point is 1/3 stocks, 1/3 bonds and 1/3 switch your currency. I then deviate depending on conditions. Switch your currency means a combination of commodities like gold and copper plus actual foreign currencies that protects against both inflation and a sharp decline in one’s home currency.

-

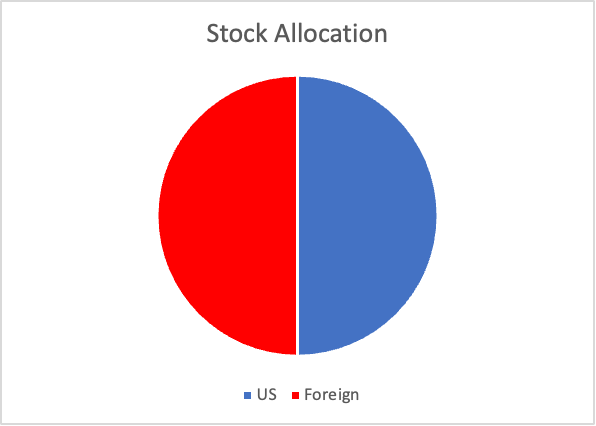

Stocks. I own more stocks than my typical. I think we are in a gradual, post-Covid recovery that will be good for earnings and the alternatives, bonds, are generally unattractive. Half my stocks are foreign as I worry about how expensive many US stocks are.

In the US, I am concentrated in banks, tech and oil. Each sector has its own dynamic. A bank borrows short term and lends long term. To over simplify, as the difference between these interest rates (short and long) rise, a bank makes more money. That’s what is happening now. Oil is unrelated (diversifying) to other stocks (more below) given the substance they produce as a profit is an expense for most other businesses. My US tech exposure is about 5% of my total portfolio. Given a roughly 20% exposure to US stocks, if they fall 20%, I lose 4%. I can handle that even if I won’t like it. The above stock allocation is very different than the typical asset allocation a financial advisor recommends. That is a separate discussion.

-

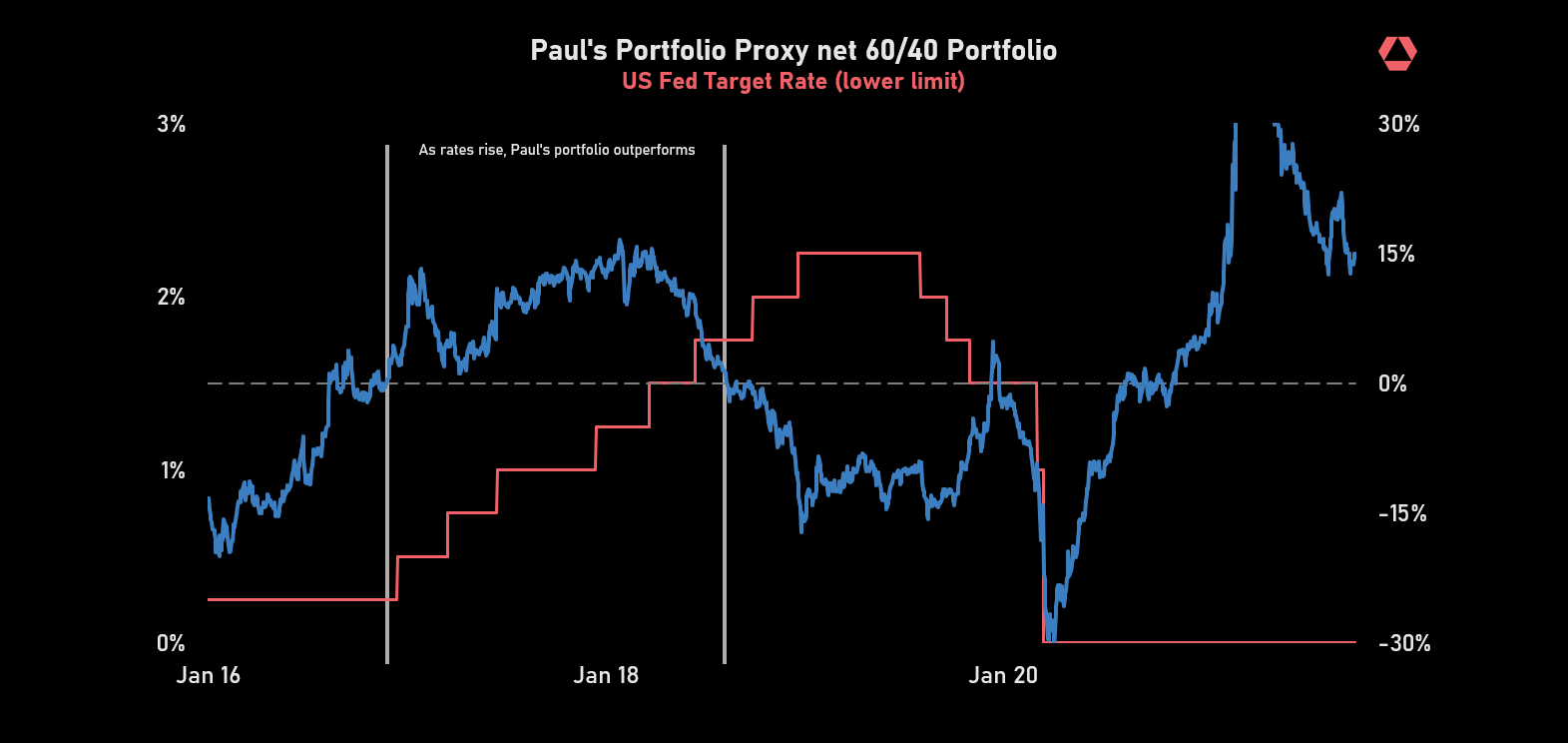

Bonds. I hold less bonds than normal and no US government bonds. The real interest rate on bonds is solidly negative. Effectively, I have to pay the US government for them to borrow my money. I own foreign government bonds, some of which are in emerging markets, and securities with higher yields from US government insured borrowers. I partially hedged the risk the Fed raises rates by going short the interest rates they might increase. In other words, short-term US bonds are unattractive to own but attractive to hedge. The chart below shows the type of scenario I worry about. It shows this current portfolio (minus the hedge) drawn back through time during a recent Fed rate hike. It loses a lot of money.

-

I have more than 1/3 of my money in “switch your currency.” This is reflected in outright exposure to foreign currencies (36%) but also in my exposures to real estate and commodities. Recognize if you buy a foreign stock, you own the stock and the currency. There are two things driving my switch-your-currency-bets. First, global warming will drive increased demand for raw materials to mute the impact, like flood control and air conditioning, which are commodity intensive. So too is green energy. Many of these stocks also provide high dividends, which provides some income. Second, given stimulative policy in the US and generally less stimulative policy abroad, the relative attractiveness of foreign currencies and hard assets is higher than average.

-

I have exposure to both an equally balanced asset allocation, a number of hedge funds and credit managers. This is me outsourcing some of the money management to others.

-

My overall exposure is above 100%, meaning I use modest amounts of leverage in my portfolio. That is also a separate discussion.

-

As the facts change, my asset allocation changes. Most of this is liquid, meaning I can sell it in a day. Fingers crossed.