Substack Library

GlossaryPolicy Error Vortex

March 23, 2022Of the almost 8 billion people we share this earth with, very few have much power over others. At this moment, however, three people have inordinate impact over our lives and wealth—Putin, Powell and Xi. Each took a big bet with a deeply flawed assumption. While each is pursuing their own agenda, together their actions are now triggering a self-reinforcing downward vortex of policy error. In response, I anticipate higher interest rates and declines in the price of many stocks and houses.

Putin

Of the three, Putin’s big bet—invading Ukraine—is the most obvious. Given roughly 10,000 dead Russian soldiers and the implosion of Russia’s economy, his policy error is glaring. His flawed assumptions—weak resistance, enthusiastic reception, able Russian army—are enumerated daily, so I won’t belabor them here.

Going forward, there is a range of possible outcomes. One of them, however, is rage. I am not a psychologist, but underwent a crash course in personality disorders for my book, Raising a Thief. Putin’s constant lying and utter lack of conscience are key warning signs.

If the Russian army continues to struggle, Putin may feel cornered and can lash out in any number of terrifying ways including chemical, nuclear or cyber. The big point is that he will not give up easily, and can be far more violent and malevolent than expected. The stock market, which bounced as we became a bit numb to the invasion, does not seem to be factoring in this possibility. Moreover, the longer the invasion lasts, the more production of wheat, oil and natural gas can be disrupted. This is inflationary and relates to Powell’s challenge.

Powell

Powell is the chief the US Federal Reserve. He decides how much money is in the world. I say the world because the dollar is the currency not only for the US, but also plays an influential role in global markets for capital. In recent years, Powell faced a number of surprises: a long period of low, even too low, inflation, a pandemic and now a war.

Even for the chief of the central bank, inflation is tough to understand and predict. Technology, relations with China, expectations, housing supply/demand and many other factors shape inflation. Powell was worried about a protracted period of prices being too low. The pandemic crushed the economy, exacerbating his deflation fears.

He tried to help by printing A LOT of money. This did what it normally does which was boost real estate and the stock market, which are both now very expensive relative to history. However, printing, protracted supply chain problems, the war and other forces have driven US inflation up to almost 8%! Unlike Putin, Powell recognizes he made a mistake and is now trying to quickly reverse course. We are going to see a very rapid withdrawal of liquidity, which the financial markets does not yet seem to have grasped.

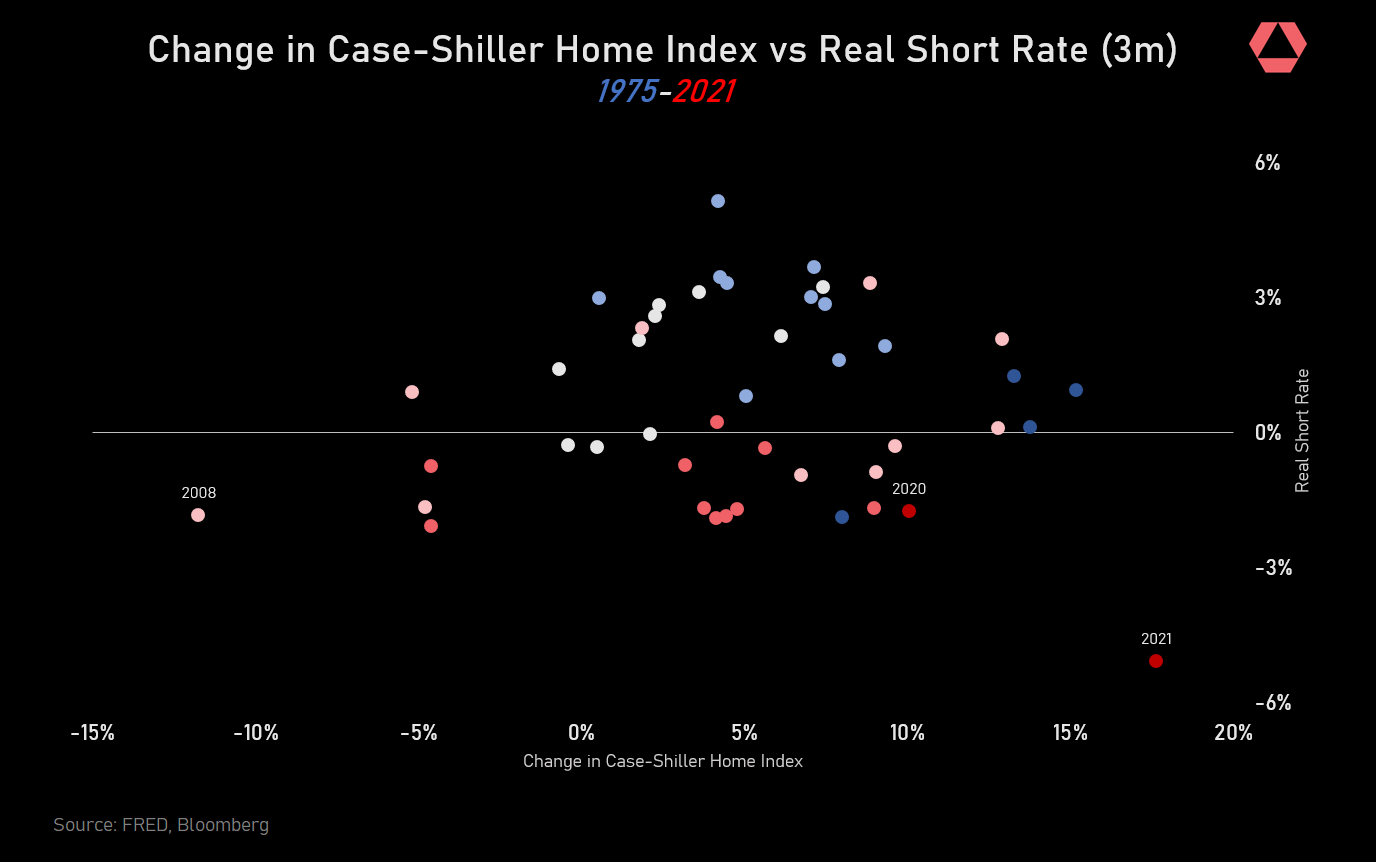

Many people don’t pay attention to interest rates, particularly real (after inflation) interest rates. But this interest rate is the force that sets the pricing of stocks, housing, venture capital, stock options and much else. We are seeing a massive divergence between real interest rates and asset prices. If real interest rates normalize or even partially normalize stock and real estate prices can fall a lot, as the charts below from Rose Technology show. The price one pays for stocks (the PE) is high because the real short rate is literally off the chart.

A normalization could lead to a very big decline in stock prices. NOT INVESTMENT ADVICE.

And housing prices may move in tandem.

Xi

Xi’s made two policy errors, which compound and exacerbate Putin and Powell’s errors. First, Xi adopted a zero-Covid policy for too long and stuck with vaccines that have inferior technology and effectiveness. Second, he placed a big bet on Putin rather than the West. Not coming out against Putin’s invasion is a sharp contrast to how his predecessor responded to 9/11.

Xi’s error about Putin probably makes Putin bolder, which means the war can get even nastier. Xi’s error about Covid means that the supply chain disruptions will get even worse, driving inflation yet higher, forcing the Fed (Powell) to reduce liquidity even more.

Policy makers in China realize there is a problem but, and this is critical, policy makers in Russia were likely very much against invading Ukraine. A number of current and former senior Russian officials (like Dvorkovich and Chubais) have indicated as much. The point: China has smart policy makers but in a system controlled by one person, their influence is limited, meaning China can get further off course under Xi.

It feels like we are on the edge of a market/geoplotical vortex and that the worst is yet to come for Ukraine, asset markets and US/China relations. Any one of these errors is a challenge, all three at once are a real mess.

(A note on pricing. These posts started off as an experiment. Now I know there is an audience. I intend to increase pricing next month given what I have seen about who is interested in detailed asset allocation information. If you would like to get the paid version but have financial constraints, reach out).

Asset Allocation

I’ve continued to adjust my asset allocation to the circumstances, trading more than normal. Below is the portfolio I hold today. This portfolio is now up 1.2% on the year, worse than where I’d like to be but better than the stock market. THIS IS NOT INVESTMENT ADVICE. As subscribers you get a window into my thinking.