Substack Library

GlossaryThe Nest, the Soul and the Calculator

November 7, 2021If you are new to Things I Didn’t Learn in School, my name is Paul and I am a writer and an investor. If you click here, you can see what these posts and accompanying podcast are about.

Numbers imperfectly capture reality. For instance, we measure each minute the same and experience some as fleeting and others as interminable. The same is true when it comes to real estate; buying property probably doesn’t make sense strictly in terms of numbers but might make sense from the perspective of emotional safety, family memories and community.

A younger reader asked about how to think about a real estate purchase, thus today’s post. I made my first real estate investment because owning a home made my wife, who grew up in the cramped Soviet Union apartment, happy. In other words, pure emotion. All money decisions are emotional, but housing is different because:

1. Unlike buying a stock or a bond, you will live inside this asset. The word house is different from “home.” The oldest tales, like The Odyssey, are about finding your way home. For many, buying a property is also, frankly, about reproduction. Salmon meet in the cities and spawn in the suburbs.

2. Buying property generally costs more money than a buyer has, which both means they need to borrow and the relative impact of this decision is much larger than other financial decisions.

In a follow up of this post, I will share some calculations I use to judge if real estate is cheap or expensive. Before getting to those, however, it’s important to disaggregate the moving pieces in real estate.

The Moving Pieces

1. The price of a house or an apartment, like anything else, is determined by supply and demand, both of which fluctuate. A property can be further sub-divided into the physical structure and the land itself.

2. In the aggregate, real estate tends to rise in value over time, mostly due to inflation.

3. In the specific, however, real estate prices are very much contingent on local conditions in which there is enormous variation. You’ve probably experienced moments where something statistically unlikely occurred to you. For instance, as a teenager, I almost froze to death on a camping trip in the second worst storm West Virginia recorded. Freak storms happen in real estate, too (like a pandemic).

4. In addition to real estate price fluctuations, an investor is exposed to the following, all of which are unstable:

-

Income. That is what you will use to pay off the debt. Income is unstable, while the debt is not.

-

Debt relative to your other assets.

-

Borrowing costs, which fluctuate.

-

Liquidity. It is possible to be “rich” with real estate but “poor” in terms of cash.

5. If you buy with debt, you are locked into a series of transactions. If your job is fine and real estate prices gradually climb, all is well. If these variables start to work against you, pain can spiral. Imagine a stock market crash (your assets fall), that leads to your layoff (your income falls) and hurts appetite for real estate, your house price falls. Boom, you are in a snow-storm.

History and the Future

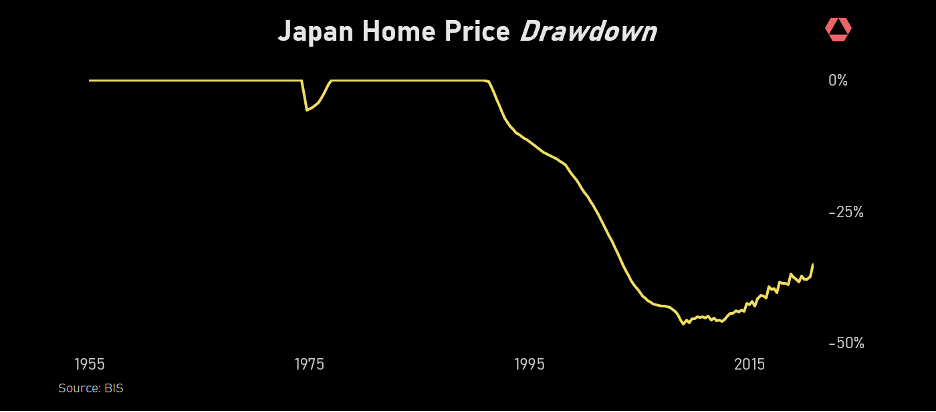

The typical advice to novice stock market investors is to buy an index, like the S&P 500, because betting on an individual stock (which also has a lot of moving pieces) is way too hard. With real estate, that’s not possible for the typical investor. You have just one house or apartment.Anticipating shifts in housing supply and demand is tough. The classic example of this is Japan. They experienced a massive real estate bubble in the 1990s and thirty years later … houses are still under water as the chart from Rose shows (thank you, Rose!).

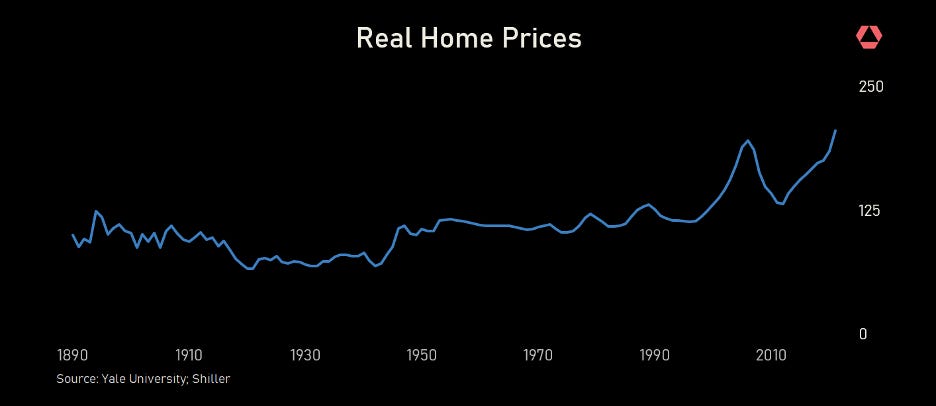

A less well known but even more compelling example is the US. As Yale University’s Robert Shiller points out, from 1890 to 1990 the real (inflation adjusted) prices of US houses … fell. Cars allowed people to move to the suburbs and home construction became more efficient. In other words, supply increased so prices fell.

Note that since then, however, US housing prices have shot up in real terms. There are two reasons. As real interest rates have declined everything has gone up. And in the pandemic, many scrambled for housing.

Yet this might not last, both because the central bank (the Fed) will reduce the amount of money circulating and, as the virus ebbs, remote work has freed us from tying our residence to our work. Why endure bad weather if you can hopscotch elsewhere? If you have kids in schools, this is impossible. But for everyone else? There is now a vast real estate arbitrage of moving to places with decent weather but bad employment and cheaper real estate. No one knows exactly where this will net out. It’s also worth noting that politics can radically shift prices. There was a booming commerical real estate market in … Latvia. Then came the Nazis, followed by the Soviets. Not good for real estate.

What Isn’t Captured in Numbers

To be sure, housing has its advantages. Having a mortgage forces you to save. Owning property anchors us to a community. I am reminded of Eudora Welty’s story Death of a Traveling Salesman. On his death bed, he realizes he never put down roots. Many families have priceless memories tied to their modest summer cabin on a lake. Real estate can also help you hedge against inflation (as long as local supply does not increase) and in certain countries, like the US, there are tax advantages to owning.

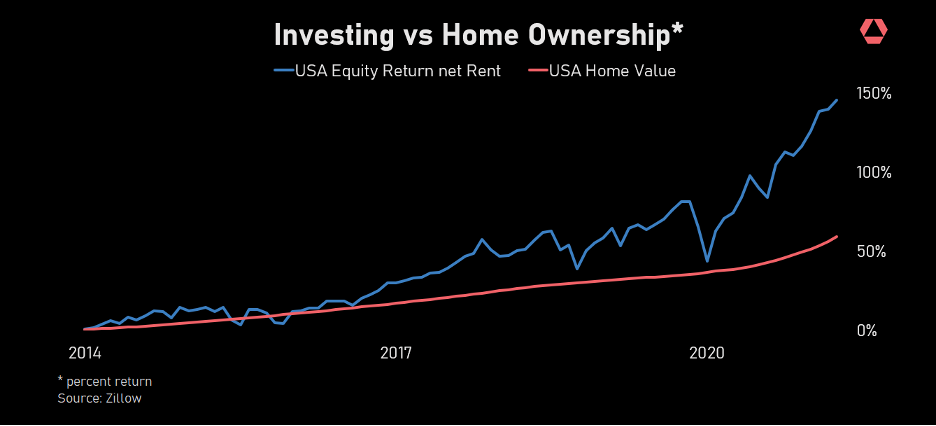

Yet, financial analysis shows most Americans who own a house now would have been better off renting and putting money in the stock market, as the chart below shows, in part due of course to the fact that stocks have gone up so much.

On Wednesday, we air a conversation with Jim Comey. I think you will find the interview fascinating. If you read these posts regularly, forward them and download the podcast—become a paid subscriber or a sponsor. I think you now have a sense of what we are up to and your financial support is an indication you value our efforts. To those that are already supporting my team, thank you! Any comments or questions, you know where to find me, paul@paulpodolsky.com.