Substack Library

GlossaryPoking Holes in the Growth Narrative

December 19, 2025Not investment advice.

Growth is going to pop, soon, because of a big tax cut coming, de-regulation and AI. Everyone knows it. Position now. Except…that’s mostly what people were thinking in 2017, ahead of the last Trump tax cut. It didn’t work out as expected, just like the tariffs have not played out according to script. Relative to the consensus of solid global growth and sticky inflation, the bigger risk is that the rate of change is slowing, just when central banks and investors believe it is about to accelerate.

In more detail.

-

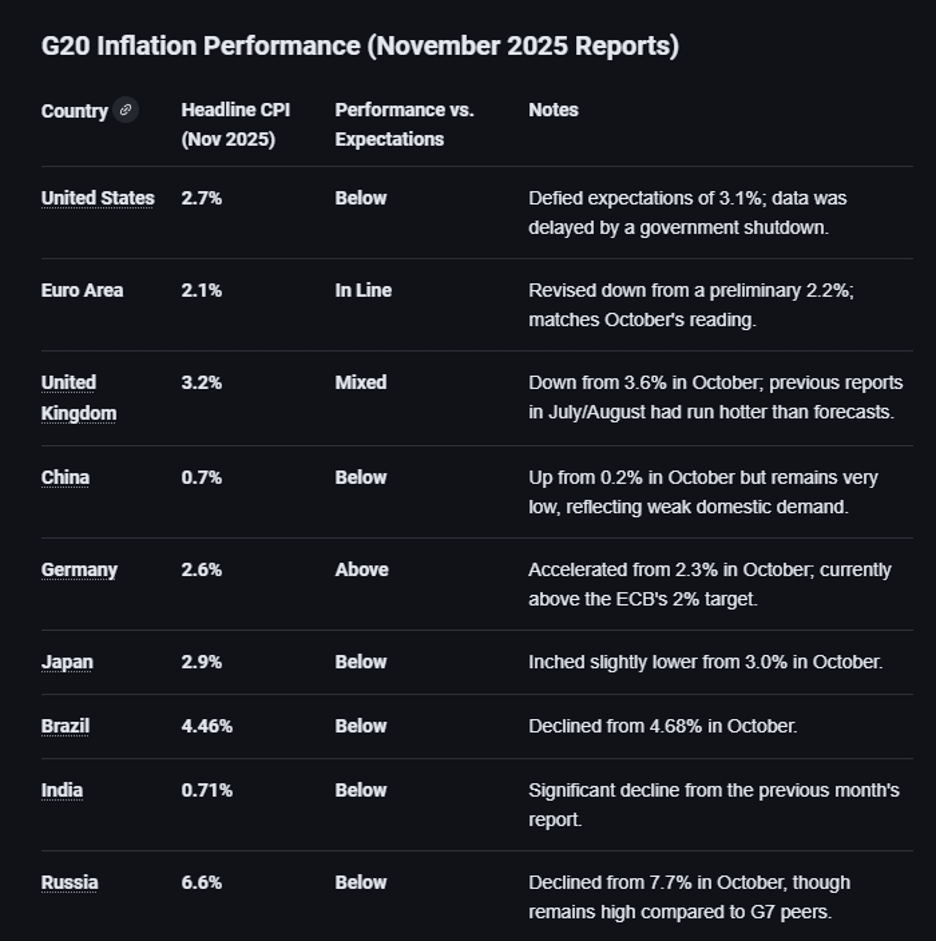

This week, we found out that US unemployment is higher than expected and inflation is lower than expected. The inflation number was 2.6%, which is a data error. However, the slowing of inflation is real. For reference, I asked Google Gemini to summarize recent reports on G20 inflation. Outside of Germany, where fiscal stimulus is active, inflation is flat or falling.

-

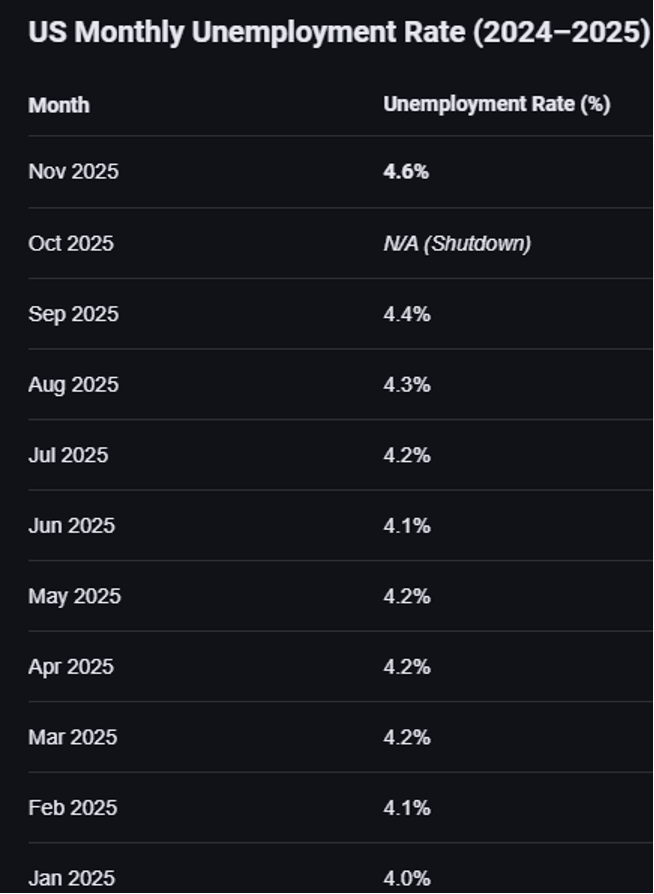

Weak employment is also a reality. US employment has gradually increased.

Stock prices have increased but that does not equate to a boom. The boom is not occurring for three reasons:

-

Monetary policy has not been very stimulative. Although the Federal Reserve is cutting interest rates, the rates that US consumers face are not changing much. Ten-year Treasury yields are higher since the Fed cut rates, due to the US fiscal pressure. Mortgage rates have decreased slightly as the difference between mortgages and Treasurys has narrowed, but the overall impact of easing is muted.

-

Fiscal policy has tightened. Tariffs were known to be a bad idea, and they are proving to be just that. Tariffs raise costs, irritate consumers, create uncertainty, and may be deemed illegal.

-

Much of the capex boom ends up abroad. The AI boom is creating wealth for equity holders and, disproportionately, foreign companies (TSMC) that make the chips needed to power the change. The actual impact on US wages is, if anything, negative.

-

Enter the One Big Beautiful Bill. Optimistic estimates assume it will boost growth. However, those estimates have assumptions. Some spending is indeed stimulative, such as border funding. No taxes on tips may or may not be stimulative, as cash tips are already largely unreported. Allowing businesses to depreciate capital expenditures is taken from the 2017 bill, which led to no meaningful capital spending. Firms wrote off past capital investments, took the windfall, and bought back stock. This was beneficial for the 1% of the population that owns 50% of the US stock market but not aggregate demand. Also, many US households will see higher health care premiums in 2026. So the fiscal looks, net net, to be a wash.

-

-

AI capital expenditures will boost growth, but not significantly, in part because the market is punishing firms when they need to finance the capex. If wages are growing less quickly due to higher unemployment, borrowing is not increasing meaningfully, and the fiscal is subdued, what will accelerate growth?

-

If growth slows, the Federal Reserve will have to cut rates more than people anticipate. The consensus is that they are done. Maybe.

-

The White House monitors markets, too, and a possible surprise in 2026 is extra fiscal stimulus in the form of a tariff rollback, blamed on the Supreme Court ruling. However, this would negatively impact the long end of the US yield curve (because tax collection would fall). In short, the government does not have much ability to stimulate the economy in most countries because of the poor fiscal situation. Either AI creates a boom, soon, or the economy will decline.

-

A note to readers: I will take some time away from these weekly notes to write some for Kate Capital clients. I will also be in Brazil doing research the week of January 12. If enough Brazil subscribers want to gather, we will find a time. Contact Julia@katecapllc.com if you are in Brazil and interested.