Substack Library

GlossaryWhat Changed

February 5, 2026Not investment advice.

The momentum went out of the market. What shifted?

-

Since Warsh was announced as the new head of the Fed, stocks have declined five days out of six. Perhaps the White House effort to neuter the Fed backfired. Warsh got the job he always wanted, but he is the least dovish of the people who were up for the job. Will he truly be hawkish once he is in the chair? That seems less likely, but it is also true that his calls on inflation in 2008 were bad and wrong at at time when the debate on future inflation is robust.

-

Earnings have been strong, well above expectations, but the amount of capital expenditures from the Mag7 is higher than expected. The more capex, the less share buybacks. Less buybacks = more shares on the market = less bullish stock market. The spending from the cash-flow-generating companies (like Meta and Google) might be big enough to put OpenAI out of business. Maybe the spending is even designed to do so. What happens to OpenAI’s backers if it collapses?

-

The capex spending so far is reaping benefits. Google’s earnings were great, and it doesn’t take more than a click on your browser to see that their AI engine is powerful. How will AI impact companies? It is a complex question, and it is easier to go sector by sector, company by company, to know. This then creates uncertainty—what stock is safe?

-

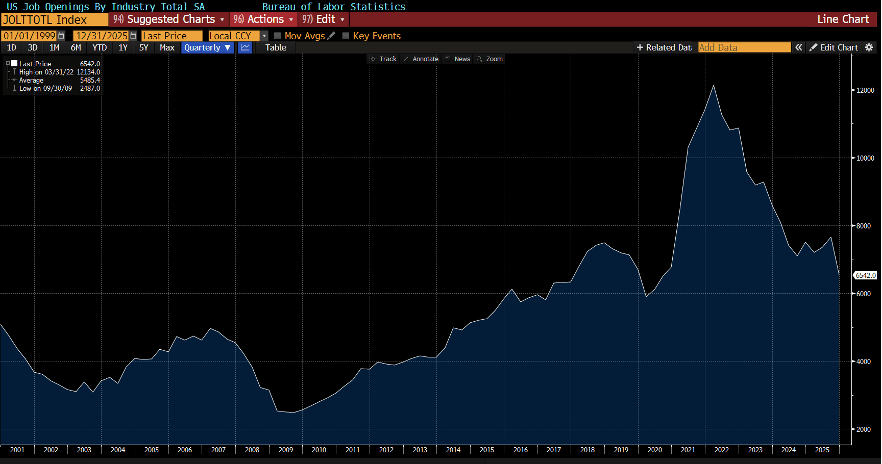

We know that there are two parts to the US economy: a wealthy upper tier responsible for most of the discretionary spending, and everyone else. The “everyone else” part of the economy is weak. Job openings are at their lowest level since COVID.

The upper-income part is highly tuned to the stock market, which is now negative year to date. If this continues, the momentum in the US economy can switch quickly.

-

Valuations of US stocks have been in the 99th percentile for a few years. When valuations are extreme and the investment community is max long, small shifts can cause big downward adjustments in price.

-

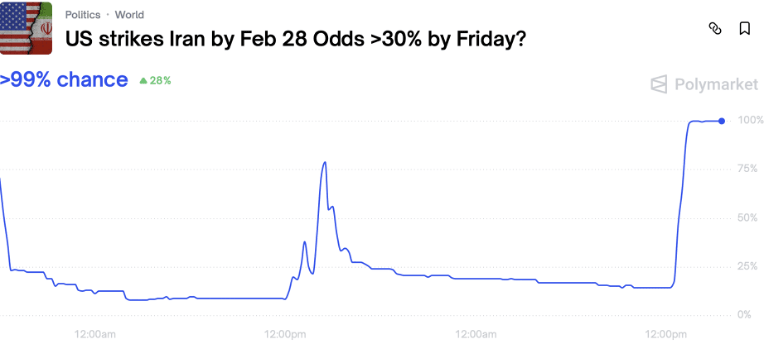

There are at least 50/50 odds of the US attacking Iran. The odds on Polymarket are 100%.

-

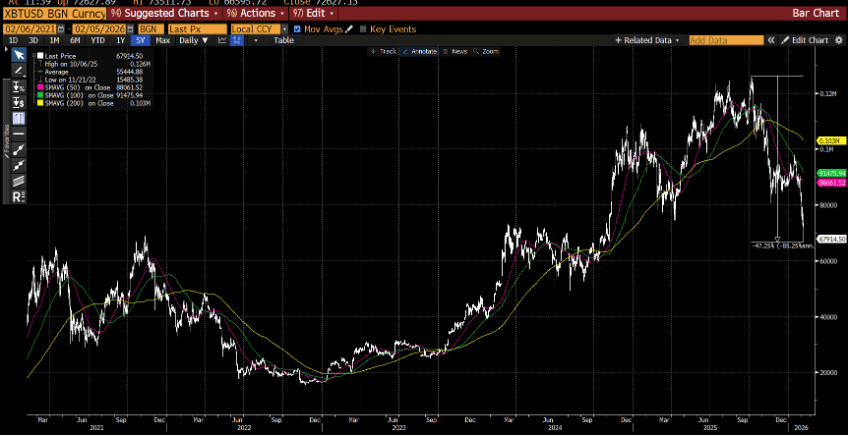

Bitcoin has fallen almost 50% and is now back to where it was when Trump took office. About 25% to 30% of the US population owns some form of Bitcoin. In Europe and Japan, those numbers are smaller, more like 10%. In any case, there is a wealth effect impact. This also may be a symptom—are households selling Bitcoin to raise cash?

-

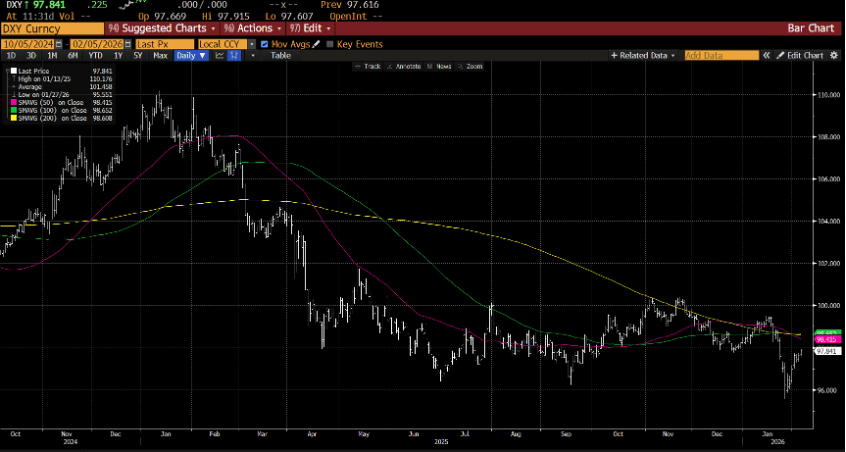

Rule of law in the US is weakening, though much could change depending on how the mid-term elections go. The US dollar has weakened about 7% since the changes began, a far cry from an emerging-market-style sell-off. But that may be because it is hard for people to adjust their mental model to see the US as a weak rule-of-law country.

-

If stocks don’t bounce, then there are billions and billions of dollars of program sellers that begin to sell stocks, so it can feed on itself. All else equal, the above leaves me more bullish on bonds and less bullish on stocks.

-

So what changed? It was not one thing. It’s a lot of smaller things hitting at once. The “Fed is easy” narrative took a hit on the cusp of a potential regime change in Iran, along with reduced buybacks and a collapse in crypto—when the market is long stocks and short bonds—forcing investors to reverse positions, in turn causing a scramble and price adjustment.