Substack Library

GlossaryWhere the Facts Stand

February 19, 2026Only craftsman copy: artists create.

Isaiah Berlin, 1947

Not Investment Advice.

Is the US going to bomb Iran? I don’t know. I also don’t know what the US is seeking to achieve. Yes, the world would be a safer place if Iran operated more like Switzerland, but how does bombing it change that dynamic? So I put those questions to the side and focus on what I can understand, the facts.

-

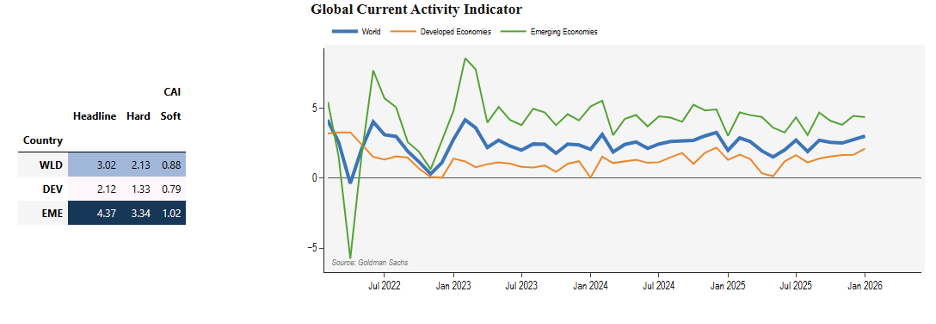

Growth is solid.

Source: Goldman Sachs

-

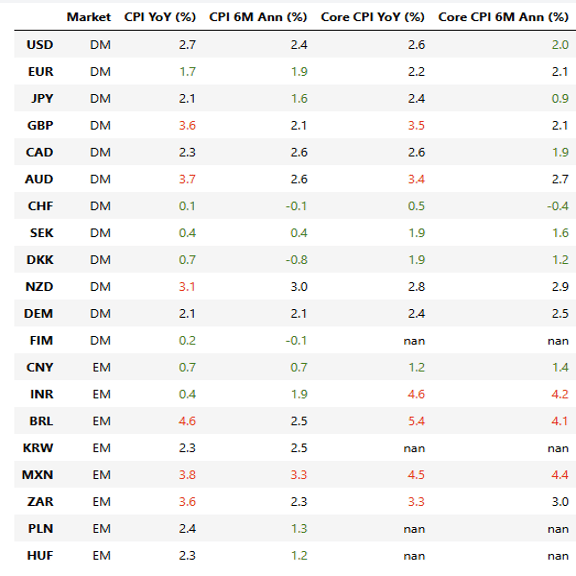

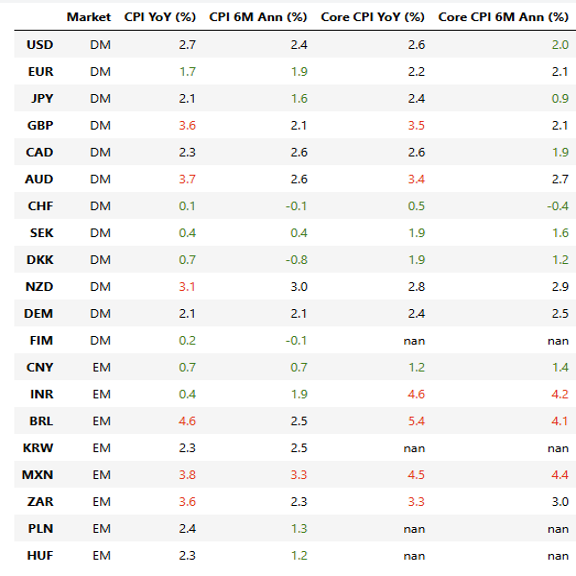

Inflation, as I mentioned last week, is quiet. Easing last year led to a pickup in growth but no rise in inflation, which is good.

-

Yield curves (10-year bonds vs. 2-year bonds shown below) steepened in recent years, and are now stable. That creates a floor. Below I show the yield curves of the US, Canada and Germany. They all look the same.

Source: Bloomberg

-

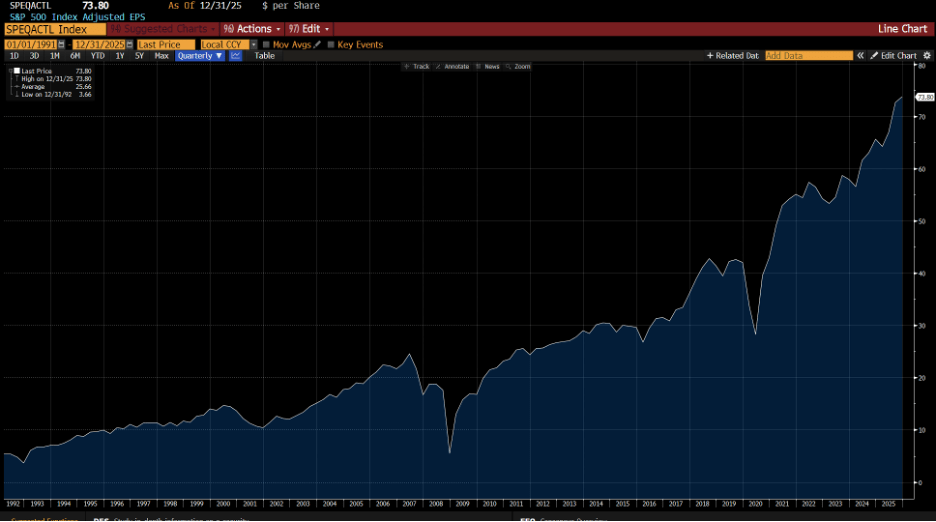

Stocks are expensive (97th percentile) and earnings are solid. Below is EPS, earnings per share. Note the negatives in 2008 and 2020. No sign of that here. Inflows into stocks are seemingly on automatic pilot; P/Es of certain blue-chip stocks have detached from reality, meaning even strong earnings can only lead to mediocre or even negative returns for widely held stocks. If the momentum in the US stock market slows, so too, rather rapidly, will economic growth.

-

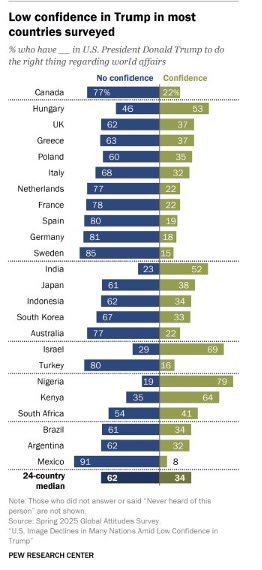

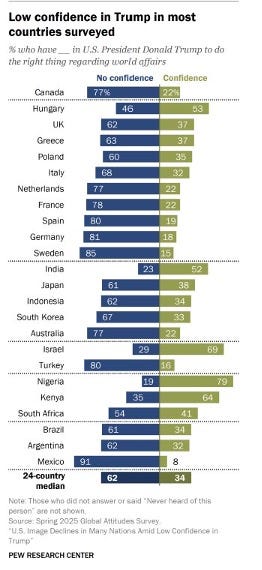

The US needs to attract a lot of capital to keep the dollar stable and according to Pew, the world doesn’t like the US as much as it used to, so presumably they will be less enthusiastic about investing here though, looking at the (TIC) inflow data, the money still seems to be flowing but investors are “hedging” their exposures (creating modest dollar selling).

-

Dollar bearish is bullish for rest-of-world assets. Looking at the world from China’s perspective, they probably feel under attack and need to build an even deeper moat. That’s driven a move in gold and, if the US does go after Venezuela and Iranian oil, China’s oil supply gets more uncertain. Though of course cutting off Russian supply, a chunk of which goes via the East Siberia-Pacific pipeline, isn’t possible.

-

China’s stranglehold on heavy rare earths (as opposed to light rare earths) remains a countermeasure, as do their holdings of US Treasuries. Heavy rare earths are indeed concentrated in China. Brazil is not a substitute. The key ingredient is “ion-absorption clay deposits.”

-

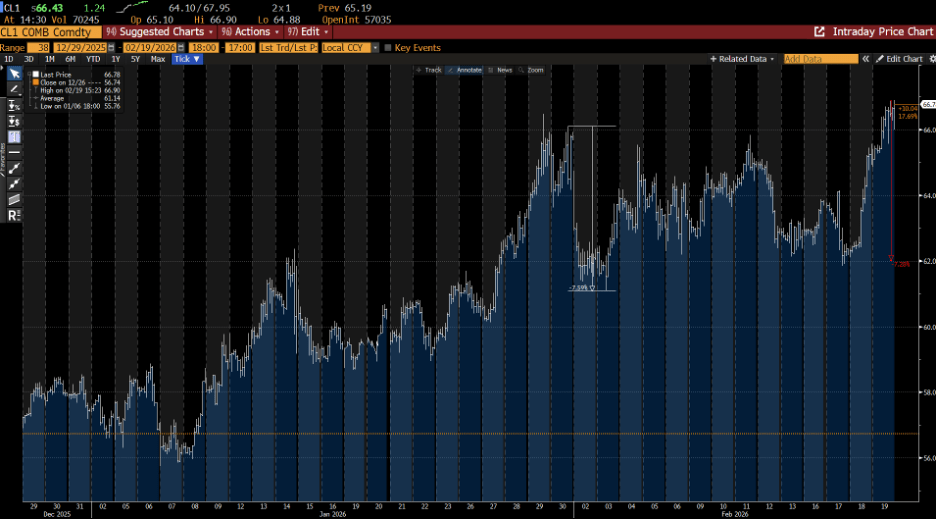

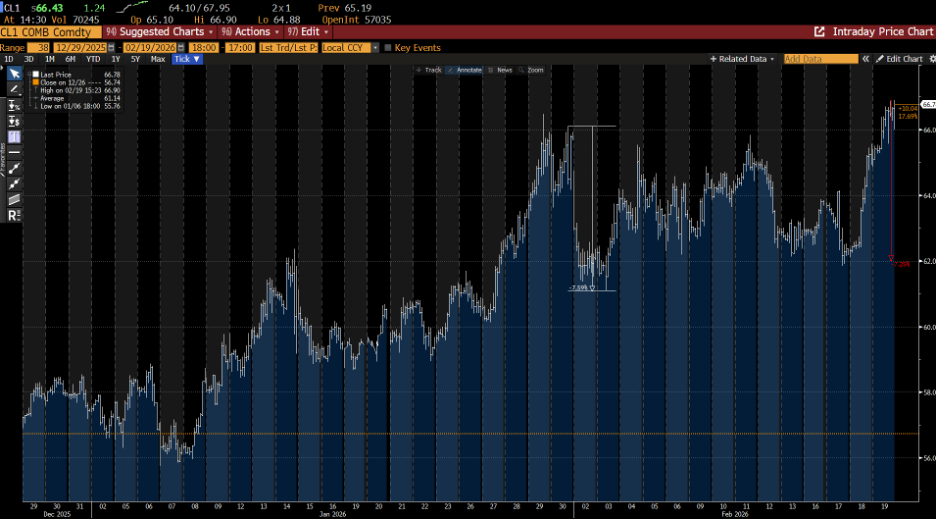

For these medium-term forces to play out, we must get past Iran. Oil has been grinding higher this year but each weekend the US doesn’t attack, the price sinks.

-

The moment oil prices rose this week, other markets ground to a halt. Rallies were sold, sell-offs bought. The decision of whether to attack boils down to one person. Likely Iran is another intermission in the same old story, though of course there are low odds of a catastrophic series of miscalculations. Meanwhile, companies make money, AI gets better, inflation grinds lower. A more fundamental decision comes in November, when the US ability to smoothly transition power via the voting booth will undergo a test. But that’s too far ahead for markets to process right now.

-

One closing thought—I wonder if AI will reduce market volatility over time. The ability to quickly synthesize information is improving exponentially. This might lead to faster price discovery and less volatility. I don’t normally go “oh wow” over new technology, but the latest tools elicit exactly that reaction.

This document is strictly confidential and is intended for authorized recipients of “A Letter from Paul” (the “Letter”) only. It includes personal opinions that are current as of the date of this Letter and does not represent the official positions of Kate Capital LLC (“Kate Capital”). This letter is presented for discussion purposes only and is not intended as investment advice, an offer, or solicitation with respect to the purchase or sale of any security. Any unauthorized copying, disclosure, or distribution of the material in this presentation is strictly forbidden without the express written consent of Paul Podolsky or Kate Capital LLC.

If an investment idea is discussed in the Letter, there is no guarantee that the investment objective will be achieved. Past performance is not indicative of future results, which may vary. Actual results may differ materially from those expressed or implied. Unless otherwise noted, the valuation of the specific investment opportunity contained within this presentation is based upon information and data available as of the date these materials were prepared.

An investment with Kate Capital is speculative and involves significant risks, including the potential loss of all or a substantial portion of invested capital, the potential use of leverage, and the lack of liquidity of an investment. Recipients should not assume that securities or any companies identified in this presentation, or otherwise related to the information in this presentation, are, have been or will be, investments held by accounts managed by Kate Capital or that investments in any such securities have been or will be profitable. Please refer to the Private Placement Memorandum, and Kate Capital’s Form ADV, available at www.advisorinfo.sec.gov, for important information about an investment with Kate Capital.

Any companies identified herein in which Kate Capital is invested do not represent all of the investments made or recommended for any account managed by Kate Capital. Certain information presented herein has been supplied by third parties, including management or agents of the underlying portfolio company. While Kate Capital believes such information to be accurate, it has relied upon such third parties to provide accurate information and has not independently verified such information.

The graphs, charts, and other visual aids are provided for informational purposes only. None of these graphs, charts, or visual aids can of themselves be used to make investment decisions. No representation is made that these will assist any person in making investment decisions and no graph, chart or other visual aid can capture all factors and variables required in making such decisions.