Substack Library

GlossaryPressure Builds

May 8, 2026Not investment advice.

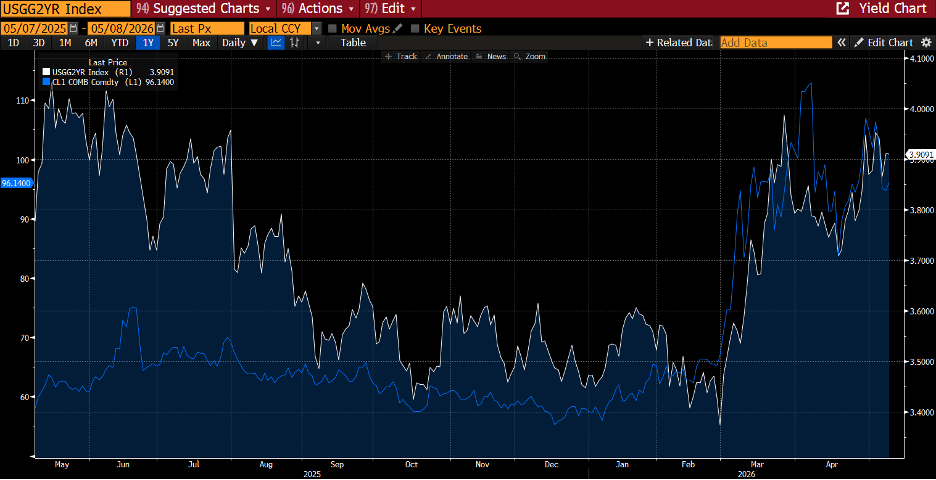

Oil is having an outsized impact on the price of all other assets. Bonds, for instance, are full of oil. Below I show 2-year bond yields (white) in the US versus oil (blue). The recent rise in bond yields is mostly driven by the rise in oil, and similar dynamics are evident in most markets. That’s why the whiff of a possible compromise in Iran matters a great deal.

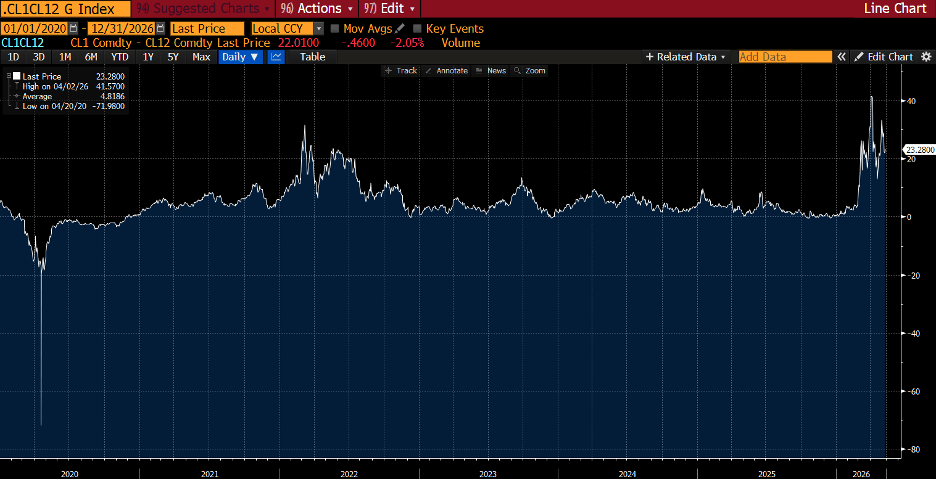

The market is pricing the war will continue. The clearest evidence for this is the premium at which oil delivered soon (like next month) trades relative to oil delivered next year. Nearby oil is trading at a premium similar to what you saw during the early days of Russia’s attack on Ukraine, as shown below.

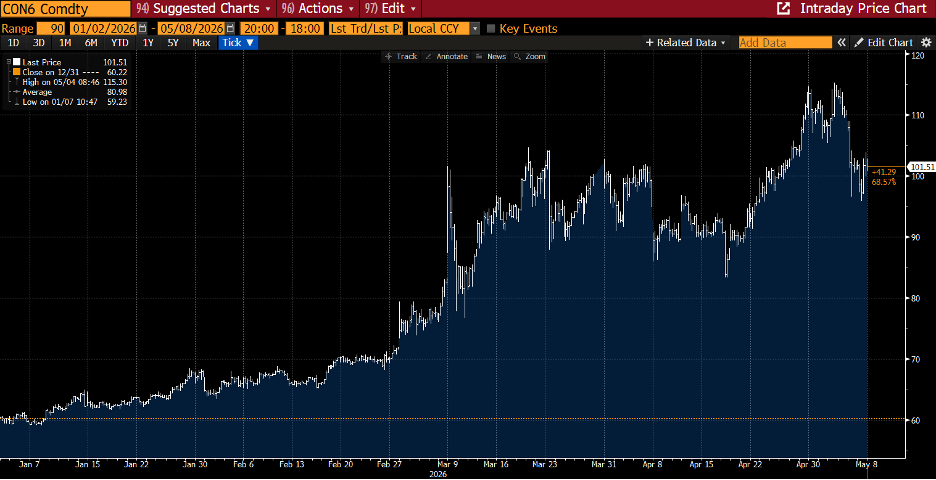

Mechanically, to keep prices this high, speculators need buy a lot of oil futures because producers (people who own the oil coming out of the ground) are selling oil to lock in these high prices. So far, these two sides are roughly offsetting. Since the initial lurch higher in prices in March, oil prices have roughly gone sideways. The passage of hundreds of ships through the Strait, increased US production, and the shipment of oil via alternative means (like a pipeline from Saudi Arabia) also help.

No one is privy to what everyone is thinking, so we need to guess. Given the risks, even signing a one-page memorandum will be seen as progress.

Here is how I see the perspectives of the different players:

1. China, the GCC, and the G20 want the Strait to open. China wants its oil, the GCC wants to export, and no G20 leader wants to face voters irate over rising prices. Because China is Iran’s most important client, China’s public affirmation this week of its support for negotiations is important. But it is also nuanced: China also wants to see the US lose.

2. The US is almost desperate. Energy prices are high, inflation is rising, Trump’s popularity is ebbing, and even some MAGA faithful don’t like the war. Gasoline can jump from $5 to $10 a gallon if the Strait does not open soon. Israel has said it doesn’t want to end the war until the current Iranian regime falls, but the US can agree to a deal with Iran even if Israel doesn’t like it.

3. Iran would like to end the war if doing so involves (a) getting paid off in the form of sanctions relief and having assets unfrozen (likely) and (b) being granted some form of control/tribute collection over the Strait, much as Egypt and Turkey retain over their respective straits (less likely). I still don’t understand how the US and Iran come to agreement on Iran’s nukes.

Iran has discovered that even if they don’t have a bomb, controlling the Strait is sort of like having one. It’s possible Iran, knowing Trump’s constraints, digs in and the worst-case scenario unfolds: a spike higher in oil, a violent sell-off in bonds that then crushes the stock market rally. But the odds appear to be shifting away from that maximalist position. Despite Iran launching missiles at the UAE and firing on the US Navy, Brent oil, as I write this, is down on the week. The market is smelling the chance of, if not a resolution, then at least an improvement in oil flows.

This document is strictly confidential and is intended for authorized recipients of “A Letter from Paul” (the “Letter”) only. It includes personal opinions that are current as of the date of this Letter and does not represent the official positions of Kate Capital LLC (“Kate Capital”). This letter is presented for discussion purposes only and is not intended as investment advice, an offer, or solicitation with respect to the purchase or sale of any security. Any unauthorized copying, disclosure, or distribution of the material in this presentation is strictly forbidden without the express written consent of Paul Podolsky or Kate Capital LLC.

If an investment idea is discussed in the Letter, there is no guarantee that the investment objective will be achieved. Past performance is not indicative of future results, which may vary. Actual results may differ materially from those expressed or implied. Unless otherwise noted, the valuation of the specific investment opportunity contained within this presentation is based upon information and data available as of the date these materials were prepared.

An investment with Kate Capital is speculative and involves significant risks, including the potential loss of all or a substantial portion of invested capital, the potential use of leverage, and the lack of liquidity of an investment. Recipients should not assume that securities or any companies identified in this presentation, or otherwise related to the information in this presentation, are, have been or will be, investments held by accounts managed by Kate Capital or that investments in any such securities have been or will be profitable. Please refer to the Private Placement Memorandum, and Kate Capital’s Form ADV, available at www.advisorinfo.sec.gov, for important information about an investment with Kate Capital.

Any companies identified herein in which Kate Capital is invested do not represent all of the investments made or recommended for any account managed by Kate Capital. Certain information presented herein has been supplied by third parties, including management or agents of the underlying portfolio company. While Kate Capital believes such information to be accurate, it has relied upon such third parties to provide accurate information and has not independently verified such information.

The graphs, charts, and other visual aids are provided for informational purposes only. None of these graphs, charts, or visual aids can of themselves be used to make investment decisions. No representation is made that these will assist any person in making investment decisions and no graph, chart or other visual aid can capture all factors and variables required in making such decisions.

xyz