Substack Library

GlossaryProductivity Shifts > Regional Wars

May 22, 2026Not investment advice.

During the railroad boom, there were regional wars, like the Anglo-Zulu War, that today almost no one remembers. We remember the railroads, however. A bridge in my town—a massive wrought-iron structure—was built in 1884 and still handles railroad traffic. The point is: for investors, the AI boom is more important than a regional conflict, despite how much attention the conflict attracts.

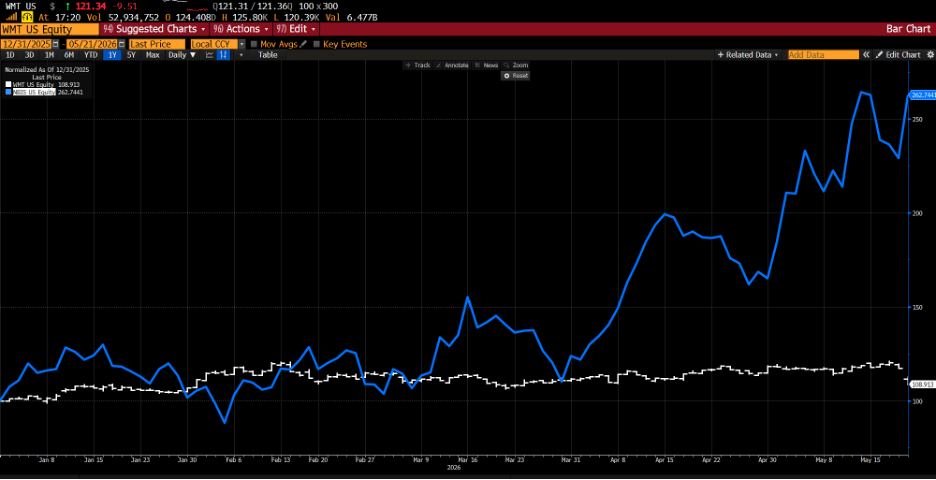

Like most of you, I am not a technology specialist. But also like most of you, I can’t understand the world without studying technology. Since launching Kate, AI has fundamentally changed the way we operate as investors—from what we study to how we study it. What’s happened to our company is happening to the global economy. To cite but one of hundreds of perspectives, compare two stocks, Walmart and Nebius. Nebius builds efficient AI data centers in the cloud. It rose 14% on Thursday and is up 162% this year, while Walmart fell on weak earnings and is now up about 8%.

The AI upcycle is powerful for a few key reasons and, I suspect, will not slow down despite the increasing likelihood of Fed hikes. Here is what is catching my eye:

-

This is a true productivity revolution. Everyone I know who uses AI, including non-tech-savvy people, is amazed by it. It’s a visceral “wow” despite us being nearly four years since ChatGPT launched.

-

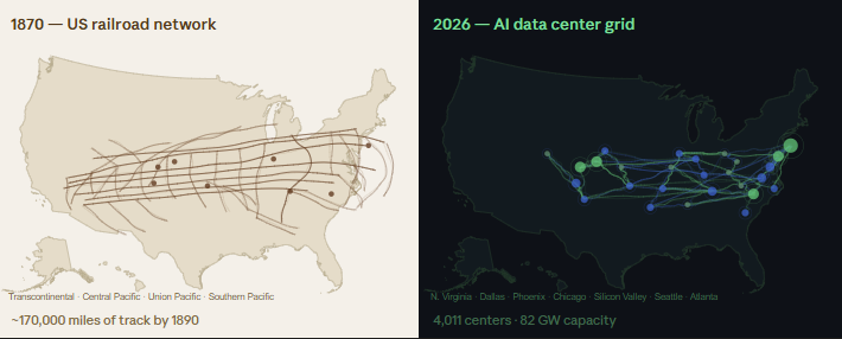

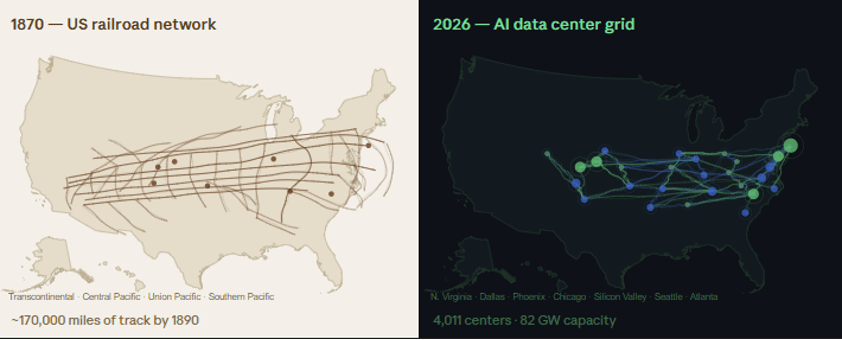

No one knows, as far as I can tell, how many of these data centers we ultimately need. Thousands are getting built and they are all getting used. I would like to know how many tokens (the basic unit of information in an AI model) Kate Capital has used. I don’t know the answer, but I know it is big. Now visualize companies all over the world doing this, and none of us—including the model makers—knowing exactly where this will stop. The AI network is a sort of cognitive rail network.

-

This is not a debt-fueled boom. The Mag 7 has taken on about $50 billion in debt against $600 billion in profits. As a result, much of their spending will not shift dramatically due to interest rates.

-

I didn’t hear much about rising interest rates or energy prices in the Mag7 (AAPL, MSFT, NVDA, GOOGL, AMZN, META, TSLA) quarterly calls. Yes, Amazon noted higher fuel prices and Apple’s CFO noted the cost of memory going up, but these were footnotes.

-

Many, but not all, of these companies hold significant investment portfolios. Google, for instance, has shares in Anthropic and SpaceX. If the environment is good for Google’s stock, it is exceptionally good for their private holdings—meaning an upswing is supercharged. That can also work in reverse if there is a downturn.

-

The US is the epicenter of these models—Anthropic, OpenAI, and Gemini (Google) are all in the US—which creates enormous strategic power. There is emerging evidence that Ukraine is doing better against Russia because it has both a numerical and technical (AI-enhanced) advantage in drones, which cause 80% of all casualties in the war. Much as better cannons determined who colonized whom in the 18th and 19th centuries, the same is now true in war. If AI helps determine who wins wars, then the US government will be fully behind the success of these companies, adding fuel to the rally. These are thus not normal companies. They are national treasures.

-

Due to the war and higher interest rates, fund managers have big “hedges” on—long their favorite stock names but short the index as a hedge. This creates a potential mismatch if the index goes up while the stocks they love go down. If they then cover the index, we could see a short squeeze.

-

A risk premium has built up on US assets due to unpredictable policy. Policy will remain erratic. But the center of the global productivity shift is in San Francisco (or driving distance from it), far from Washington, and will suck in capital from all over the world. Trying to build truly world-class AI in a place that controls thought—like China—is structurally harder, which is why they lag (even if they have cheaper costs and better access to energy). In the US, I can ask AI if White House policy is erratic and get a nuanced answer. In China, of course, plenty of questions are forbidden.

In short, the boom is bigger than the war. That’s the big picture.