Substack Library

GlossaryLearning from War

May 29, 2026Not investment advice.

The Iran war is roughly 75% over. There is approximately a 25% probability of escalation and another significant spike in energy prices.

Months in, a few key observations stand out:

1. It is wiser to trade the consequences of the war — primarily higher inflation — than to trade the war itself.

This is because:

a. There is little edge in trying to predict near-term moves by Trump or Tehran. Questions such as “How exactly will the US incentivize Qatar to pay off Iran to reopen the Strait?” or whether either side will overplay its hand are coin flips with wide bid-offer spreads.

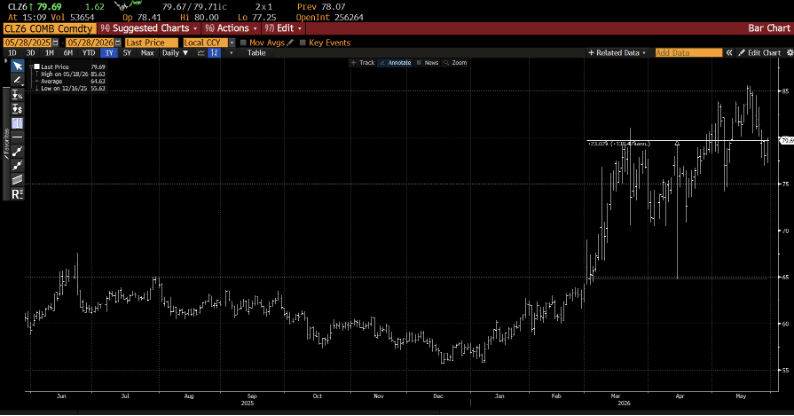

b. The oil market shows signs of informed positioning and insider trading. Large, well-timed bets have appeared ahead of key White House announcements. As a result, heavy buying of 5,000+ $110 calls this Friday afternoon triggered concern. After the initial spike, oil has gone roughly sideways for two months amid persistently high volatility — a difficult combination for most portfolios.

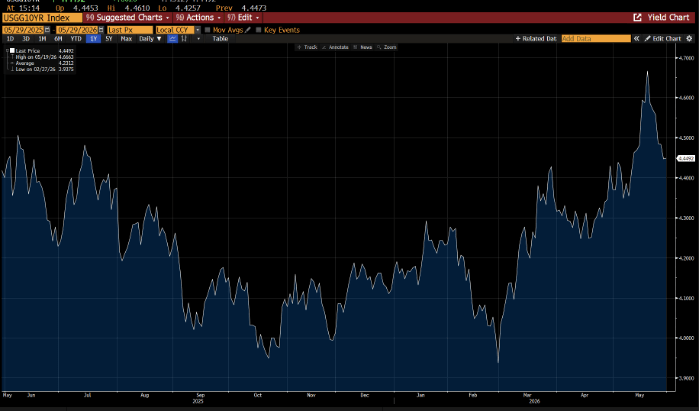

c. In contrast, the transmission mechanism from oil to the broader economy is clearer. Sustained higher oil prices feed directly into higher inflation. With oil inventories already low, the risk of another spike remains live. As bond markets have sold off (shown below) and real yields have risen, inflation-linked bonds have become more attractive as are outright short positions in nominal bonds. Markets are currently pricing inflation as ultimately contained.

d. A prolonged conflict also drives higher military spending, which is fiscally expansionary and therefore negative for bonds.

Some countries, like the US, are less exposed to the war, while others, like Europe, are more exposed. This creates the opportunity for differential bets, long one shot the other.

Even if the conflict de-escalates, the combination of elevated inflation, continued fiscal impulse, and massive AI-driven capex spending should keep upward pressure on both growth and prices.

2. The AI story is also fundamentally a military story.

a. While technology has always played a role in warfare, today’s AI represents a far more powerful leap than canals, railroads, or even the internet. AI is almost like nuclear energy.

b. The United States holds a significant structural advantage through its dominance in leading AI models and advanced chips even if it is far behind Ukraine in figuring out how to apply this knowledge on the battlefield. The US AI lead puts adversaries like Iran, Russia, and China at a clear disadvantage. However, aggressively pressing this technological edge carries risks. Hubris could provoke unpredictable counter-reactions. The more effectively AI helps the US and its allies win battles, the greater the incentive for China to act aggressively on Taiwan before the gap widens further, for instance. This at a time when the supply chain for robotics is entirely dependent on China.

c. Within the defense sector, AI is creating the same pattern of creative destruction seen elsewhere in the market. Just as software stocks were disrupted while semiconductor memory stocks surged, capital is now flowing toward next-generation defense companies while leaving legacy military contractors behind.

In short, war is now a feature not a bug and we all need to learn how to manage through such turbulence. This week, Russia sent a clear warning signal that the Baltics may be next on their agenda.

This document is strictly confidential and is intended for authorized recipients of “A Letter from Paul” (the “Letter”) only. It includes personal opinions that are current as of the date of this Letter and does not represent the official positions of Kate Capital LLC (“Kate Capital”). This letter is presented for discussion purposes only and is not intended as investment advice, an offer, or solicitation with respect to the purchase or sale of any security. Any unauthorized copying, disclosure, or distribution of the material in this presentation is strictly forbidden without the express written consent of Paul Podolsky or Kate Capital LLC.

If an investment idea is discussed in the Letter, there is no guarantee that the investment objective will be achieved. Past performance is not indicative of future results, which may vary. Actual results may differ materially from those expressed or implied. Unless otherwise noted, the valuation of the specific investment opportunity contained within this presentation is based upon information and data available as of the date these materials were prepared.

An investment with Kate Capital is speculative and involves significant risks, including the potential loss of all or a substantial portion of invested capital, the potential use of leverage, and the lack of liquidity of an investment. Recipients should not assume that securities or any companies identified in this presentation, or otherwise related to the information in this presentation, are, have been or will be, investments held by accounts managed by Kate Capital or that investments in any such securities have been or will be profitable. Please refer to the Private Placement Memorandum, and Kate Capital’s Form ADV, available at www.advisorinfo.sec.gov, for important information about an investment with Kate Capital.

Any companies identified herein in which Kate Capital is invested do not represent all of the investments made or recommended for any account managed by Kate Capital. Certain information presented herein has been supplied by third parties, including management or agents of the underlying portfolio company. While Kate Capital believes such information to be accurate, it has relied upon such third parties to provide accurate information and has not independently verified such information.

The graphs, charts, and other visual aids are provided for informational purposes only. None of these graphs, charts, or visual aids can of themselves be used to make investment decisions. No representation is made that these will assist any person in making investment decisions and no graph, chart or other visual aid can capture all factors and variables required in making such decisions.

25 Likes∙