Substack Library

GlossaryBigger Swings

November 7, 2025NOT INVESTMENT ADVICE

Swings in the financial markets are echoing the swings in politics. They both have the same source—the difficulty of digesting new technology.

Here’s what’s catching my eye:

-

Markets turned south after the Fed cut interest rates last week (October 29) but signaled it might pause further easing.

-

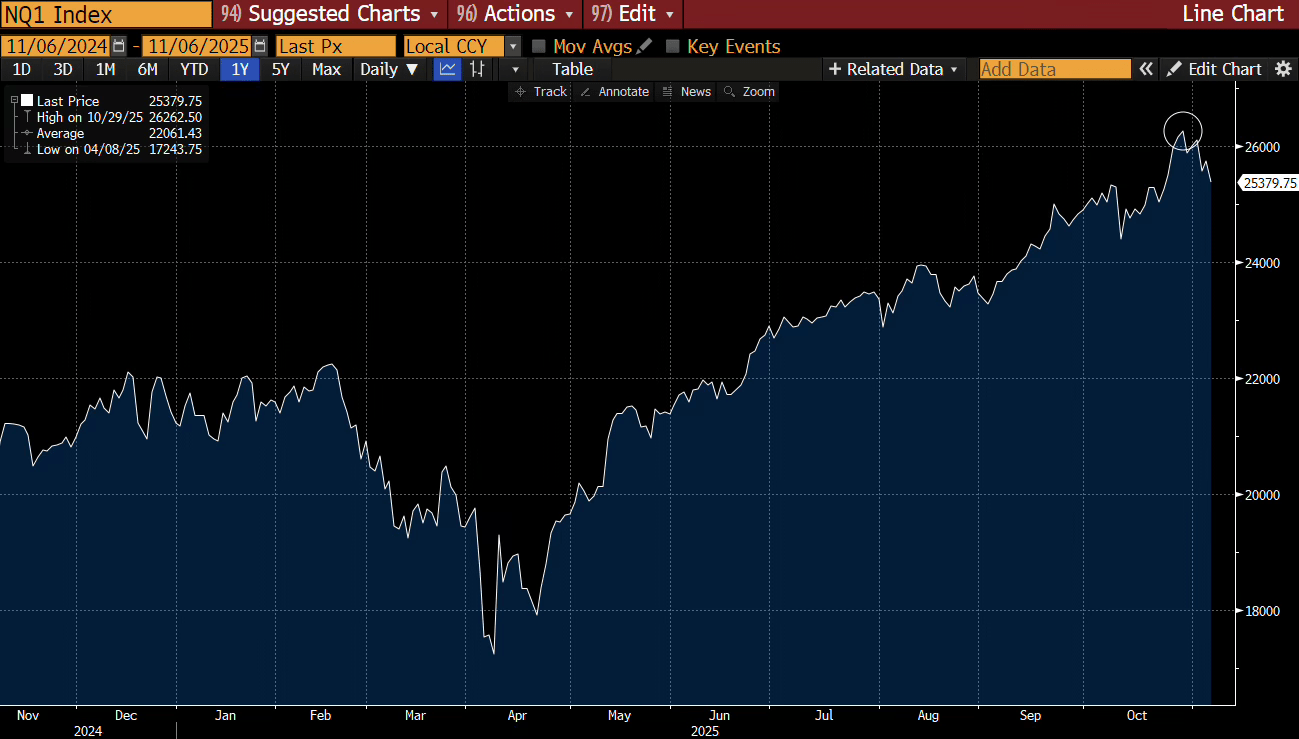

In the run-up since April, there have been multiple “tests” of the bull move, each about 3%. We are at about 3% down as I write. Either this level holds and we bounce, as in all previous times, or we break lower.

-

If we break lower, it is about market structure. Earnings are fine, even good. There are (mostly) three groups of people trading stocks—retail, professional investors, and pod shops. Retail has bought each dip. Not professional investors, who remain skeptical of the price and mindful of the Fed. The pod shops are more inscrutable but probably are playing for the next zig and zag, hunting for weak hands. In this case, if retail doesn’t buy for whatever reason (tax-loss selling?), pod shops will hit the offer, and professionals won’t buy until we are about 10% lower, at which point their internal rate-of-return models will begin to kick out buy signals. Stocks can go down, but only so far and retail does seem to be buying some.

-

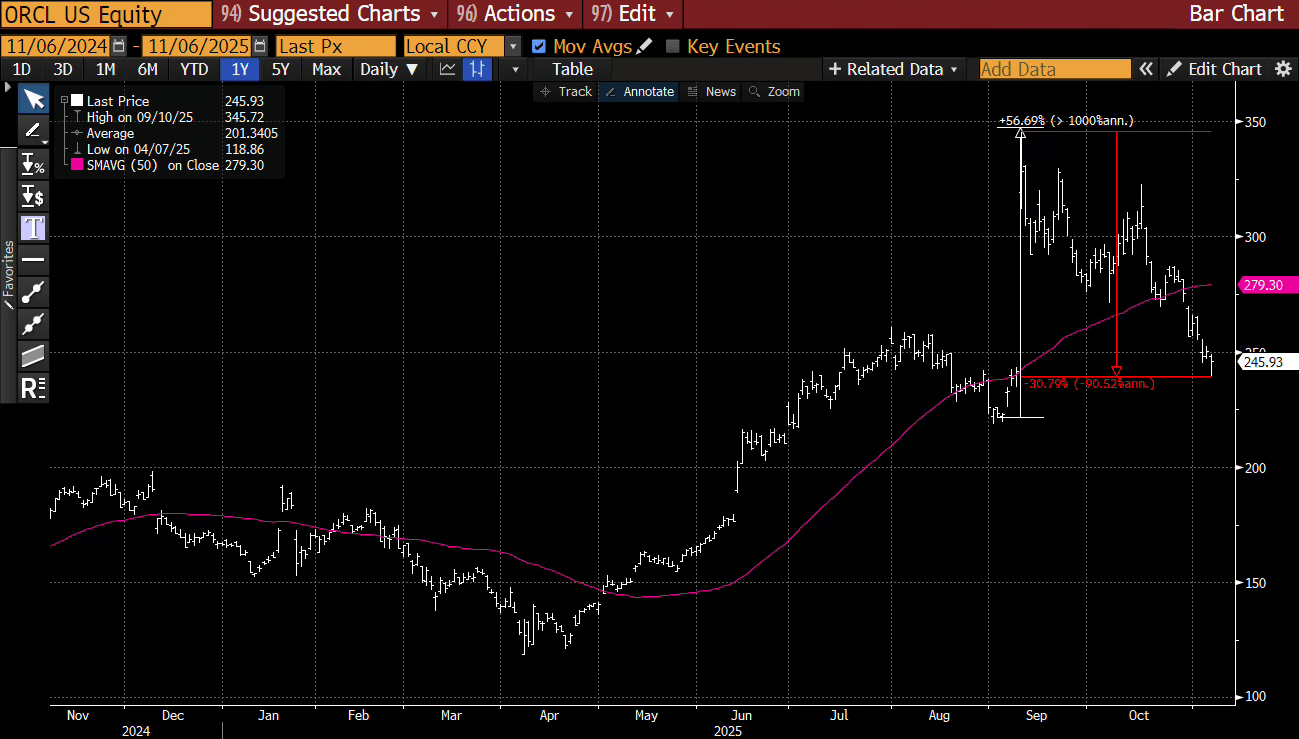

What price to attach to the tech companies at the center of the AI boom? No one can say for sure. These are five-year projected cash flows, and most analysts have trouble projecting one year out. As I noted last week, if OpenAI can charge for its services, it could become the Mag 8. If it can’t, it will lose a lot of value, and hinting at government loan guarantees is hardly confidence-inspiring. Stocks like Oracle jumped 50% in a few days after its September 9 earnings release and then fell 30%. Oracle is a fifty-year-old company that mostly provides databases—hardly a start-up—with uncertain cash flows.

-

The Fed also doesn’t know if the new technology will reduce jobs more than building a lot of data centers and tariffs will boost inflation. We will get some of each. So they wait for data to light the path, but the data machine is shut down because of the government shutdown. As investors, we need to make decisions today, however, data or no data.

-

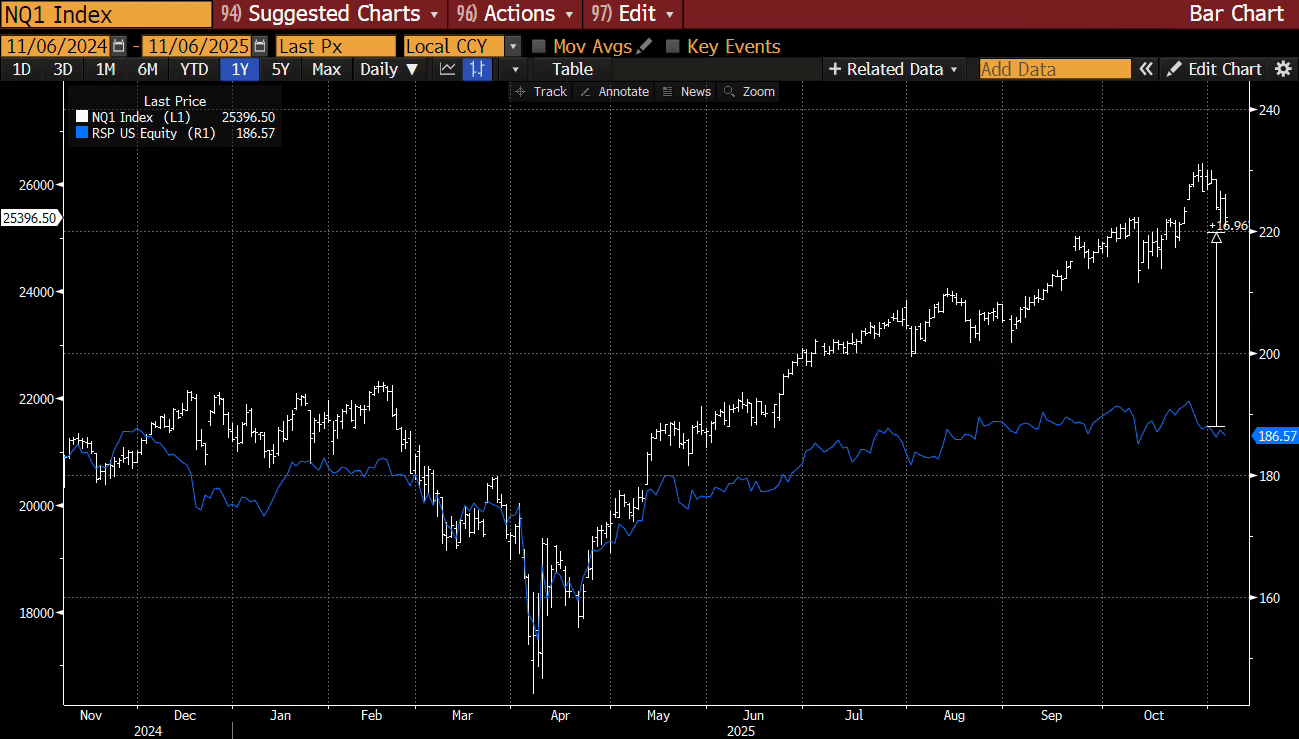

Within stocks, there have been two stock markets—the regular stock market and tech stocks (I show that below). The regular average stock stopped going up months ago. If the Nasdaq were to fall back toward the regular stocks, it would decline 10% to 15%. Other markets, like Bitcoin, are off about 15% in the last few months.

-

In addition to the Fed shifting course, so too did most other major central banks. The Bank of Canada cut rates to 2.25% on October 29 but signaled a likely pause in further cuts; the Reserve Bank of Australia and Bank of England have similarly held steady or hinted at pauses recently. In short, in a monetary-driven rally, now the monetary policy is in question. So the “tilt” on stimulus has shifted.

-

This week, the White House’s signature policy tool—tariffs—seemingly was deemed to be illegal, or partially illegal, by the Supreme Court. The verdict awaits, but the hearing was clear enough. This is bullish for stocks but bearish for long-term bonds because U.S. revenue collection will decline, though we don’t know the degree, and perhaps SCOTUS offers some partial constraint rather than a more full-throated defense of Congress’s right to set taxes.

-

The U.S. fiscal picture is more nuanced than commonly believed,. Yes, the U.S. has a large budget deficit. The U.S. spends a bit over $7.2 trillion a year and pulls in (in taxes) about $5.2 trillion a year. That means the U.S. needs to borrow about $2 trillion. A portion of that is in short-term bills. The total borrowing (absent bills) is more like $1.5 trillion, or around 5% of GDP. About $1 trillion of this is interest, meaning the primary deficit (the deficit without interest) is close to 2%. This calculation does not include tariff revenue, which will diminish this number further. If economic growth is a little stronger than expected, the U.S. deficit situation becomes less concerning.

-

The U.S. swung to the right (Trump) and to the left (Mamdani), both clever salesmen. New technology creates upward pressure on the income of the wealthy and downward pressure on the less wealthy. The appropriate policy is to be candid with the poor and tax the rich to soften the blow. But that policy will irritate 2/3 of the population, so no politician can say it. Instead, we get cotton candy ideas that play well on the campaign trail—tariffs or free bus rides—but don’t shift the core issue.

Stocks will eventually settle, and I think inflation will ebb lower. This is a positioning shakeout. Fed hawkishness is forcing a repricing in stocks, which, if they break lower, will make the Fed less hawkish.