Substack Library

GlossaryEasing > Tariffs

August 14, 2025I am in Croatia but watching. A few thoughts.

-

Easy monetary policy matters more than erratic tariff policy. While US tariffs are at about 18%, most central banks have either already eased (US, Canada, Europe, Australia) or are expected to ease more imminently (US and Australia), as Covid-related inflation gradually seeps out of the system and labor markets soften due to past tightening. In response to this easing, global stocks are up about 12% and bond yields outside of Japan and Germany are lower. Five-year US bond yields are 56 basis points lower this year and 28 basis points lower in the UK, two places with supposedly intractable fiscal problems.

-

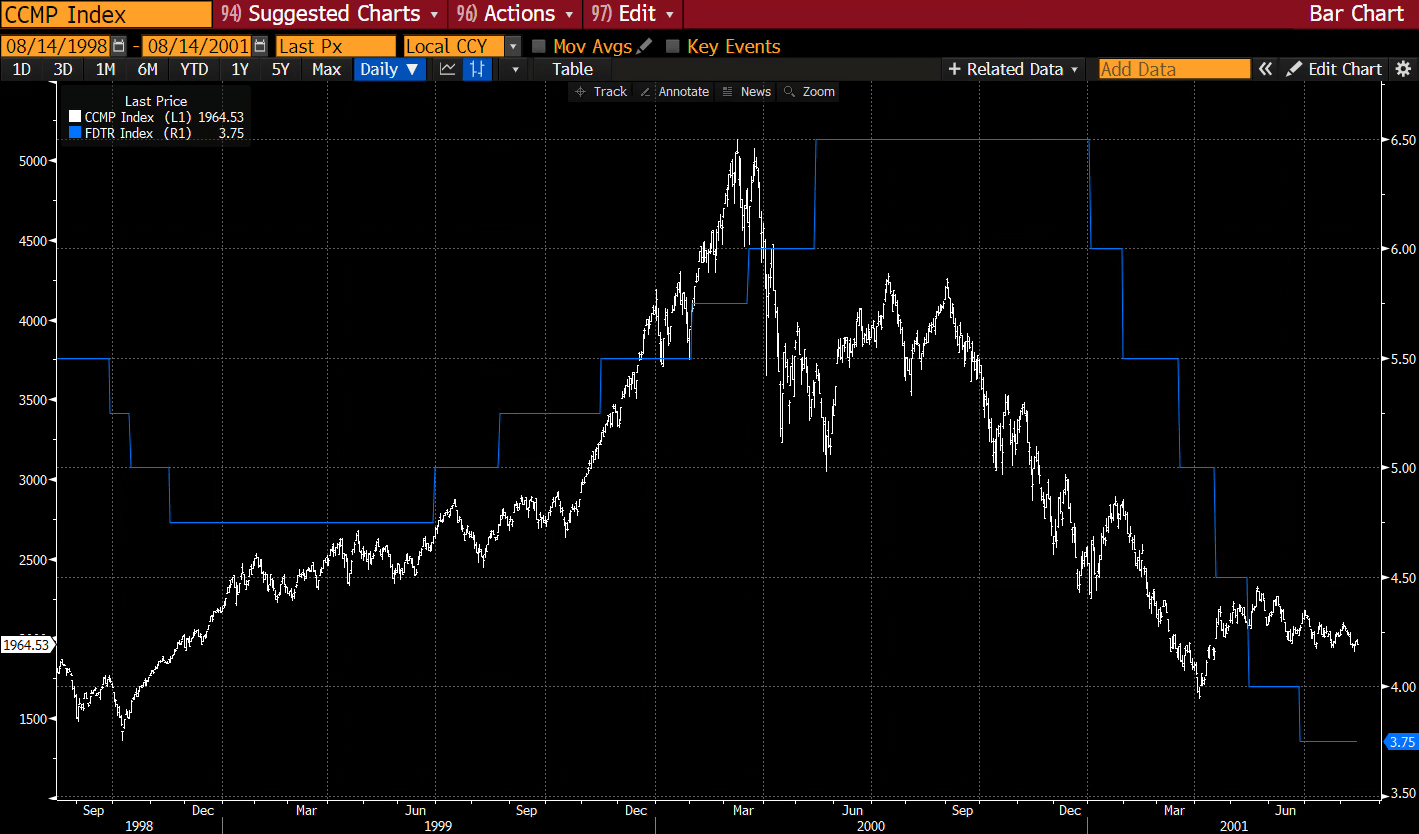

The NASDAQ is also up 12% this year and it looks like the Fed is going to ease policy next month. The last time I saw an easing with fervent tech excitement was 1998. The stock market experienced a bubble for the ages. Below I show the NASDAQ (white) and Fed Funds (blue). The Fed hiked numerous times before the bubble popped.

-

In 1999, no one living had experienced a bubble like that. The last one was in 1929. This time, a lot of people vividly remember the massive decline that followed and, as a result, are reluctant to buy. Each time the market climbs higher, it drags more people in.

-

The dollar is about 10% lower versus European currencies and about 5% lower versus Asian currencies, despite a solid rally in US assets. This is the only, muted, evidence of a global risk premium being priced for owning US assets.

This is my second trip to Europe this year. On both, the people I speak with are alarmed, even aghast, at what is going on in the US, but the impact of this sentiment seems limited to the currency market.

I will take next week off from writing, unless something very unusual happens.