Substack Library

GlossaryAdapting to Policy Uncertainty

February 16, 2025THIS IS NOT INVESTMENT ADVICE. INVESTING IS RISKY AND OFTEN PAINFUL. DO YOUR OWN RESEARCH.

Human beings adapt. A few weeks into Trump 2.0, that’s what’s happening to investors, or at least what is happening to me. The US is shifting toward a Hungarian-style, illiberal democracy. How far we shift and if we shift back are the questions.

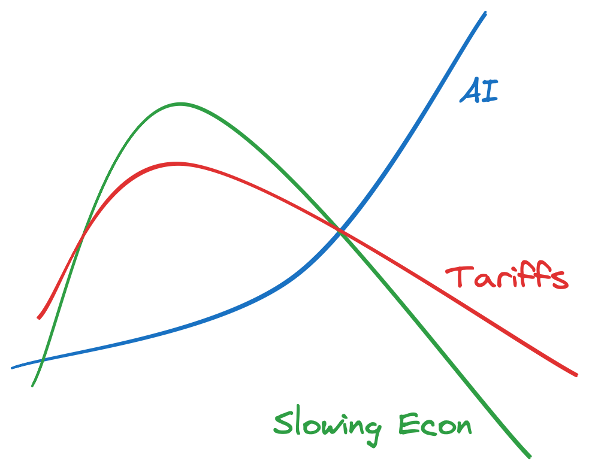

The picture in my head is this:

AI is boosting capital expenditures and productivity while at the same time softening demand for labor and will likely lower inflation. Outside of AI, growth is slowing due to high interest rates in most parts of the world (though the opposite is happening in Japan.) Policy uncertainty, most obviously Trump’s tariffs but also alliances and rule of law, is soaring, as an index from Bloomberg indicates.

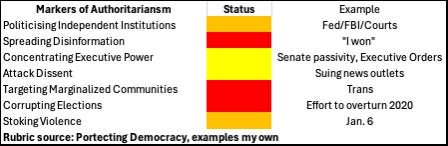

To help measure where we are, I find it helpful to have a rubric. Below is one that Protecting Democracy offers. I scored the rubric as I see these forces today. The point is many of the markers of a more authoritarian regime are either red or yellow.

Market Impact

Ascertaining exactly where we are in this shift is challenging because Trump’s policies themselves are contradictory. Trump wants to cut the deficit and taxes; he wants to protect Israel’s borders but not Ukraine’s; he wants for the US to be respected and to weaken rule of law, to hold free elections but not to lose. These contradictions reflect the contradictions in voter’s hearts. Voters want a government that gives them a lot (liberty, social security, health care, economic stability, defense) without asking a lot (taxes, rules, job insecurity, foreign aid).

Trump reads the room and adjusts adroitly. Once unveiled, tariffs led to a sudden stock market drop. Trump backed off. Reciprocal tariffs were another angle, but then a hot inflation print and polls showing voters are worried about inflation, and Trump again (this week) backed off. It was this pivot away from tariffs that led the NASDAQ to record highs Friday, which is why I keep shifting my portfolio allocations.

On the other hand, freeing January 6 rioters, and dropping charges against either convicted or charged politicians weakens rule of law. (It’s also true that strict adherence to political correctness weakens free speech, but there is a big difference between freeing a convict and a faculty staff meeting). In any event, I find it notable foreign stock markets are outperforming US stock markets and that the dollar (I show a dollar index below) is now falling. This suggests capital flows are not favoring the US.

Policy Sects

The apparent alliance between Musk and Trump is another interesting example of these contradictions. At first glance, it would appear they are aligned. But scratching the surface, their goals are distinct.

Musk’s future depends on whether he can create fully self-driving cars and sophisticated robots. He needs Tesla to beat Microsoft and Apple, not Ford. Achieving Elon’s vision requires capital and talent, but he has those already. The real challenge is regulation and interest rates. He faces one set of regulations in California, another in Texas and another in China. Automobile sales (let alone robots) also depend on borrowing costs. If rates are high, cars don’t sell. Below I show Tesla’s stock price and the interest rate of car loans. As you can see, when interest rates spike, the stock stops going up.

Now that Elon is literally in the Oval Office, he is likely finding that simplifying regulations is easier than cutting spending. At tech companies, firing people is the fastest way to cut costs. In DC, existing liabilities are the big expense; getting rid of the people that disburse the liabilities doesn’t meaningfully reduce outlays themselves. Regardless of his effectiveness, Musk’s interests are clear—simplify rules and choke off government spending to get interest rates lower.

Trump’s interests don’t necessarily align. The most glaring gap is fiscal policy, tax cuts versus spending cuts. But there are other differences. Trump wants to cut immigration, Musk wants to expand the number of visas that allow the US hire the most talented people in the world. Trump wants to contain China while Musk wants to sell there and has a factory in China. Said differently, even Trump’s closest confidants don’t align. In the coming weeks, these contradictions will be resolved and I’ll react accordingly. If Musk is influential in cutting government spending, stock and bond markets will soar. If we get a big tax cut, bonds sink.

From Here

Beyond responding as the policy evolves, I’m watching three things.

1. The markets themselves. Since Trump took power, yields and stocks are higher and the dollar is lower. This suggests the markets are looking at Trump’s expected policies as growth-positive, meaning tariff-light, but are also moving out of the US. If Trump does institute meaningful tariffs, the right portfolio is long bonds, short stocks. We repeat the 2018 market correction, meaning stocks fall sharply. If he continues to back off, it is bullish stocks.

2. Institutional erosion. The most objective measures are if the Fed loses its independence or Congress changes the Constitution to allow Trump to have a third term or an indefinite term. The 22ndAmendment, ratified in 1951, limits Trump to two terms. But Bloomberg was able to run for a third term in New York by changing the rules and Trump himself has already hinted at the same. I suspect this is part of what is driving the dollar down. If Fed independence is removed, I suspect the dollar will plummet.

-

People flows. Do people from the rest of the world still clamor to enter the US?

Initially, under Trump, I took less risk because I found the “headline roulette” hard. Now, however, I’ve become accustomed to it and look at the uncertainty as one more variable an investment manager needs to negotiate. Like I said, we adapt.