Substack Library

GlossaryAI, Employment and Salami Tactics

February 21, 2025THIS IS NOT INVESTMENT ADVICE. INVESTING IS RISKY AND OFTEN PAINFUL. DO YOUR OWN RESEARCH.

AI and a radical shift in US government policy are hitting the global economy at the same time. Together, these forces may lead to falling US employment and inflation. If that occurs, everything the trading consensus is positioned for—a strong dollar, higher bond yields and higher US stock prices—may turn out to be wrong.

AI and Employment

We know AI and robotics are changing how we operate. The question is the pace at which the AI dents demand for labor relative to the rate at which AI creates new jobs. My hunch is the hit to labor demand can happen more suddenly than people think.

One way of ascertaining the rate of change is to observe your own behavior. Twenty-four months ago, a group of enthusiastic volunteers proofread my posts. Now I use AI. Similarly, I used to build complex models to value a stock or a bond. Now my first stop is AI, which churns out models that are better than a first-year analyst.

I asked experts who comb through employment and earnings reports about the impact of AI on jobs. So far, they don’t have hard evidence jobs are being displaced even though from a commonsense standpoint, we know they are. I backed out a more hacky way to look at the question. I selected the main categories of both CPI (inflation) and employment and fed them into an AI bot and asked it what the likely changes were. As you can see, AI hits every component of CPI, often in ways I did not anticipate, like using drones to lower the cost of construction.

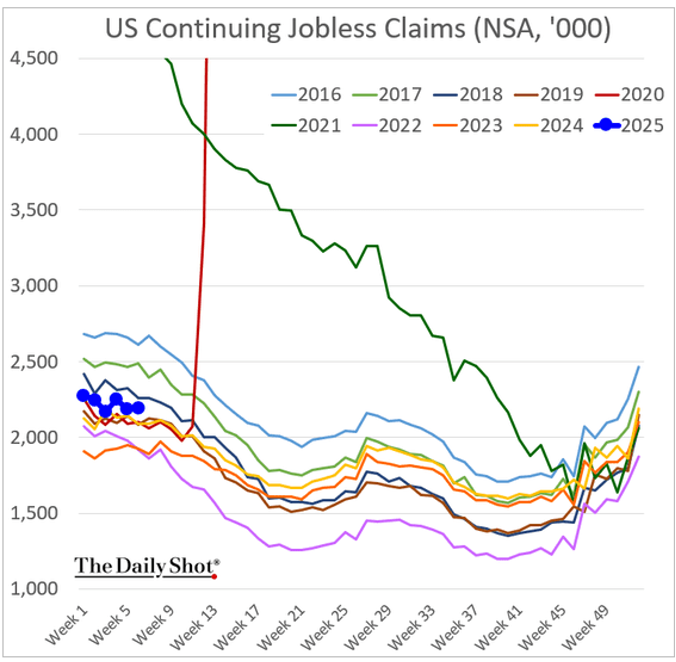

Add in to that that the Administration is firing a lot of government workers and the odds of weaker employment numbers are rising. This is not in expectations. The Fed is largely expected to have stopped easing. Note in the most recent report government jobs were 22% of the recent jobs created. That will now go flat ore even negative.

Yes, claims for unemployment are rising, but not yet sharply. However, when there are turns in data, by definition this will diverge from past data.

The Salami Slicer and Ukraine

The firing of federal workers intersects with the overall policy tilt—salami tactics. The term was coined by Matyas Rakosi, the former communist boss of Hungary. By this he meant eliminating opposition in small, seemingly insignificant steps, until nothing remained. That is what is going on in the US. Gradually rule of law is being sliced away. Examples are pardoning those convicted of January 6, freeing the convicted Illinois governor, dropping charges on the New York Mayor, reneging on signed trade treaties—the message is clear, if you are loyal, the rule of law doesn’t apply. And if you aren’t? Look out.

This same template is being applied to Ukraine, though perhaps in Ukraine’s case this is less salami slicer and more meat cleaver. Ukraine does not have leverage. They are small, poor and being attacked by a homicidal neighbor. The Administration is saying “give us your minerals, we might protect your borders,” roughly similar to the British empire in Africa. Russia has a similar rubric, only more expansive. Not only do they want Ukraine’s minerals and agriculture (the breadbasket of Europe) they want the entire swath of territory they have held intermittently for long stretches of time, thus their request that NATO pull back. This mimics the Administrations claims toward Canada and Greenland. The demands are symmetrical, though Russia has a history of killing and incarcerating their neighbors that the US lacks.

The gap with policy precedent is glaring. Recall, the US Marshall plan. In today’s dollars, the US gave $180 billion to Europe after World War II and asked in return for free trade and cooperation combating Communism, or, in plain English, the Kremlin. Now, the agenda is constricting free trade and cooperating with the Kremlin. The logical consequence of these two forces (AI/firing, and salami tactics) would seem to be less confidence in US financial markets and the dollar. Again, so far there are only modest signs of this in the prices but, by the time it is obvious, it will be too late. The ingredients for a violent reversal in pricing are increasing.