Substack Library

GlossaryAI Is Today’s Tractor

February 28, 2026Not investment advice.

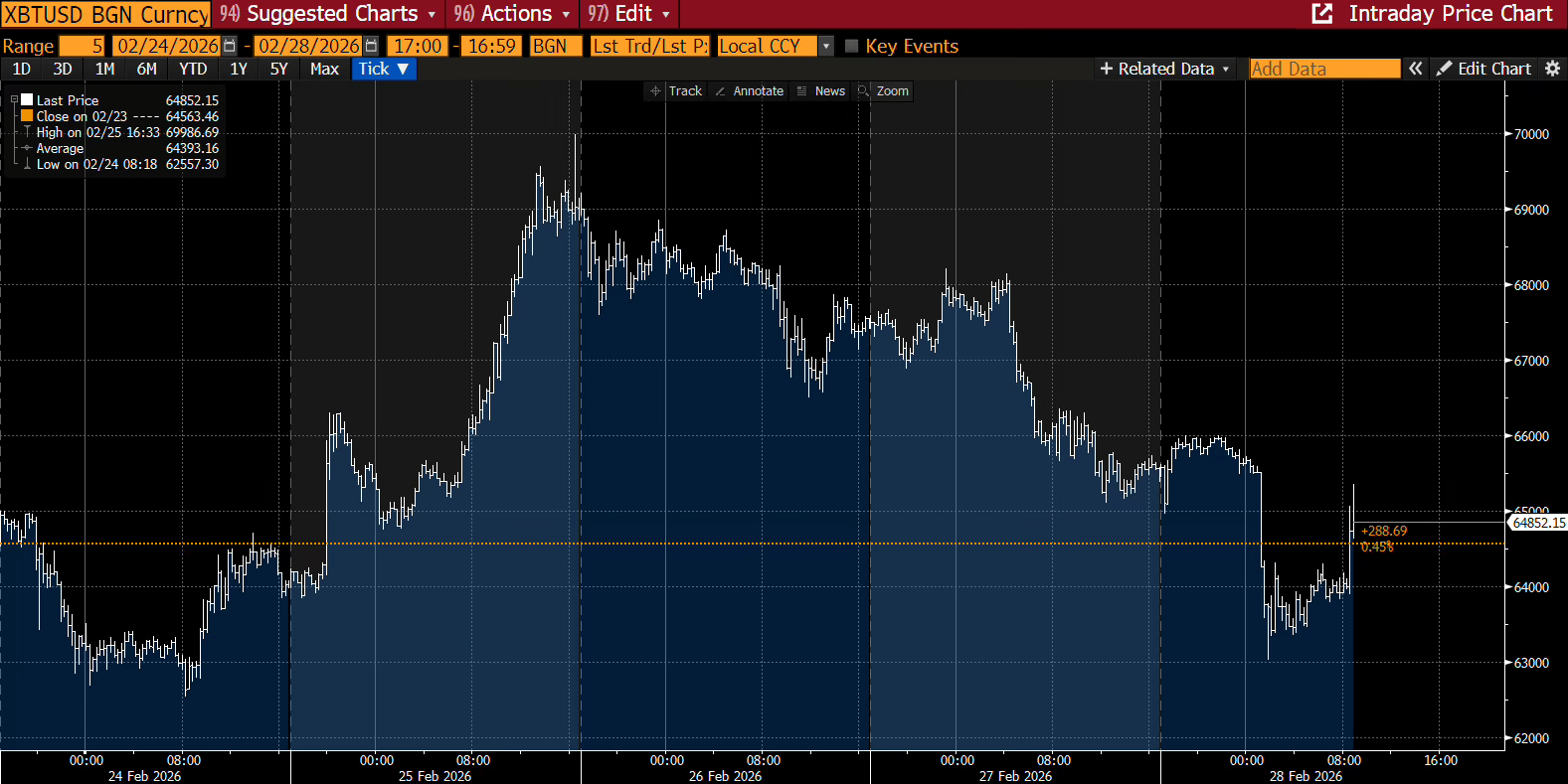

All eyes are on the war. War is terrible, the outcomes unpredictable.

The most likely moves are oil, gold and the Swiss franc up, probably the yen too. The reaction of stocks and bonds is less certain. In 1991, stocks rallied. So far, bitcoin has moved down but then up modestly perhaps following Israeli reports that the senior Iranian leadership suffered losses.

The war is unfolding against the backdrop of major, disruptive technological change.

AI is today’s tractor.

In 1900, when the majority of the global population worked on farms, the tractor was a terrifying innovation. Opponents even founded The Horse Association of America to resist the shift. In the process of freeing a population from arduous labor, mechanization overturned an economic, social and political order that had existed for centuries.

Once the order is disrupted, two things follow—enormous wealth creation and, as wealth shifts, political instability. In the last month you can see the AI shift violently rippling through all the vectors that impact us—income, borrowing, and saving and, as that happens, the political reverberation.

AI’s Impact on Income

Growth is driven by spending, and spending is fueled by income and borrowing; both are currently being disrupted. Last week’s data point: Jack Dorsey, the founder of Twitter, and now CEO of Block, fired 50% of his workforce in one day. Large cuts at Amazon, UPS and others have also been announced. Dorsey said that AI, paired with “smaller and flatter teams,” are enabling a new way of working. This will bring wealth to those that keep a job and the opposite to those that lose it.

While Block may have been overstaffed relative to its peers, the broader analytical question remains—will AI boost profits (by cutting costs) faster than it reduces income (by letting people go)? Said differently, can a company grow EBITDA per employee using AI? If the answer is yes, profit margins will grow. If it’s “no,” top line growth will falter due to weak demand. This might explain why labor turnover has ground to a halt. One lawyer told me AI has transformed her practice. “We aren’t hiring junior lawyers any more,” she said, because the functions they used to do can now be done far faster and more accurately by AI.

AI’s Impact on Borrowing

Interest rates for most borrowers are falling as inflation cools, with ten-year U.S. bond yields dropping below 4%. War with Iran will accelerate that. There are many forces driving down inflation, but technology is certainly one of them. However, interest rates for companies being disrupted by AI are rising as their cash flows deteriorate and credit quality worsens.

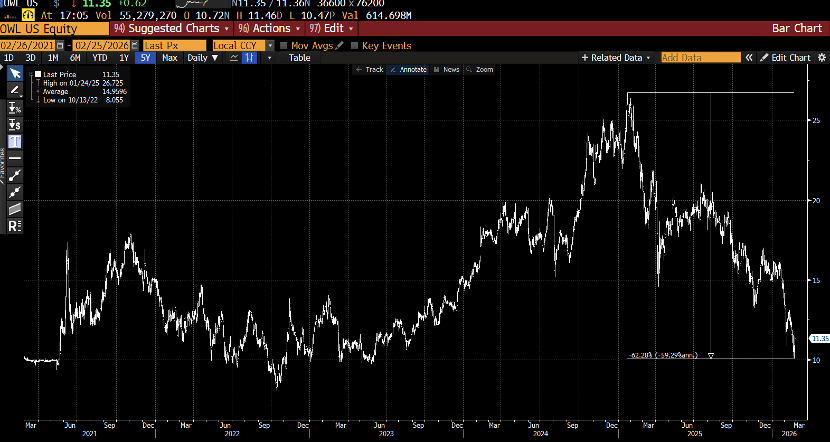

Investors have narrowed their focus to Business Development Companies (BDCs), a lending vehicle designed by Congress to support small and medium-sized businesses. While the global corporate bond market is over $40 trillion, the BDC market is small (around $450 billion). Firms at the epicenter of this shift face risks when investors pull capital from illiquid credit markets, causing borrowing costs to spike—a secondary form of disruption. Blue Owl, the firm at the epicenter of this, has seen its stock fall 60% because their investors can pull money while their assets, many of them loans to tech companies, are illiquid.

AI’s Impact on Saving

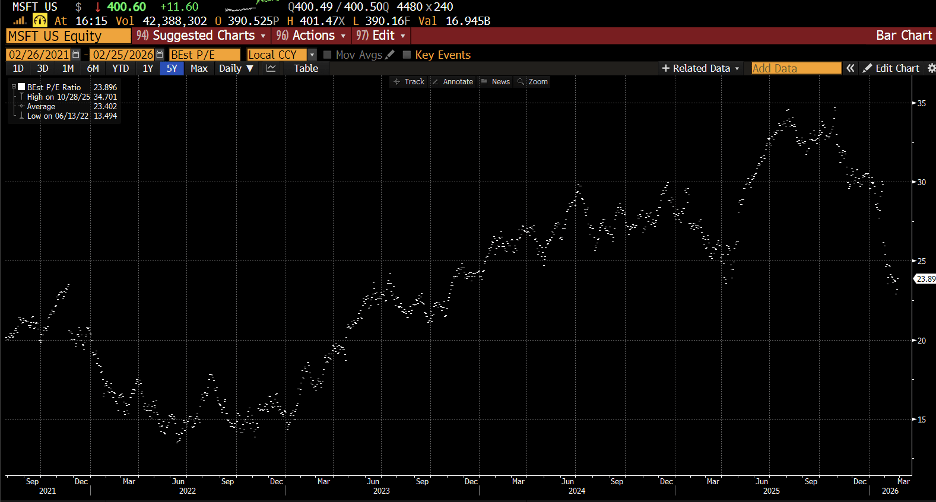

Asset prices are generally up since ChatGPT was unveiled. But investors are also punishing companies tethered to legacy processes—such as traditional HR, word processing, and insurance brokerage—fearing they cannot pivot as quickly as Block. But it’s messy. Microsoft (which owns a significant stake in OpenAI) sees its price-to-earnings ratio (shown below) compressed due to “disruption fears,” even though MSFT owns a big chunk of OpenAI.

AI’s Impact on Politics

Regarding politics and geopolitics, AI is exacerbating existing tensions, fueling surveillance states or intensifying partisan friction. The US shift in domestic politics is unsettling enough that record numbers of citizens are seeking more stable jurisdictions, as the WSJ pointed out last week. This mimics the pattern of capital flows, dollar down.

Like with the tractor, the most likely outcome is a period of lower inflation and solid profits, but also significant and sometimes terrifying employment and geopolitical disruption. Creative destruction lives on. I particularly favor liquid assets because it allows me to adjust my views and jurisdictions as the facts shift, as opposed to be locked into long-term illiquid commitments.

And as we all watch what unfolds in the Middle East, the loss of human life deeply pains me.