Substack Library

GlossaryBack To Our Regular Programming

April 17, 2026Not investment advice.

The war and the incipient energy shortage are over, just like that. There is a WSJ report the US will allow Iran to “access” $20 billion if they hand over uranium. We came perilously close to the Strait seizing up, which would have triggered a massive energy shock in products like gasoline, jet fuel, and diesel. Ship traffic is still snarled, but markets are forward-looking, and the forward-looking picture is a global disinflationary boom driven by a wave of labor-saving technology amid erratic US policy.

In more detail:

-

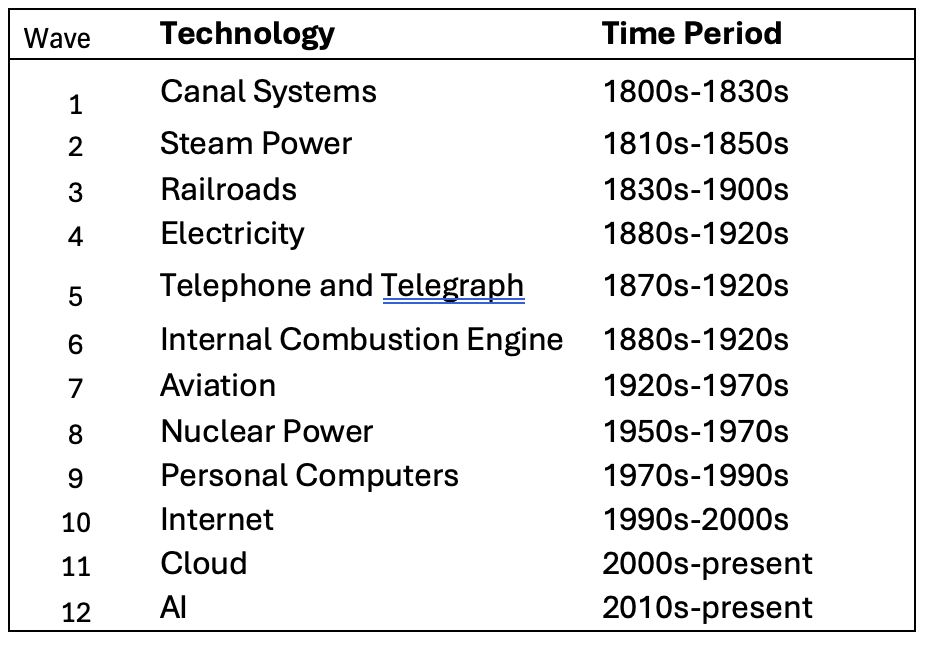

The main thing that distinguishes us from “us” 200 years ago is technology. We’ve been through waves of change and are in another one now. I notice today’s technological shift changing how I and everyone around me operate. First-hand examples in just the last 18 months include AI writing code, overhauling research, creating new employment opportunities and eliminating others, and even helping an acquaintance with screenwriting. What will the next 18 months look like?

-

Technology changes everything. In 1800, about 75% of the US population worked in agriculture; now it is around 1%. In 1800, the world’s top companies were the British East India and Dutch East India Companies. Today they are Nvidia and Google. In 1800, the top global powers were Britain and France. Today they are the US and China.

-

Everyone is now scrambling to master this technology before their competitors do. The tech is powerfully labor-saving, shifts cash flows, and is redistributing power away from the US.

-

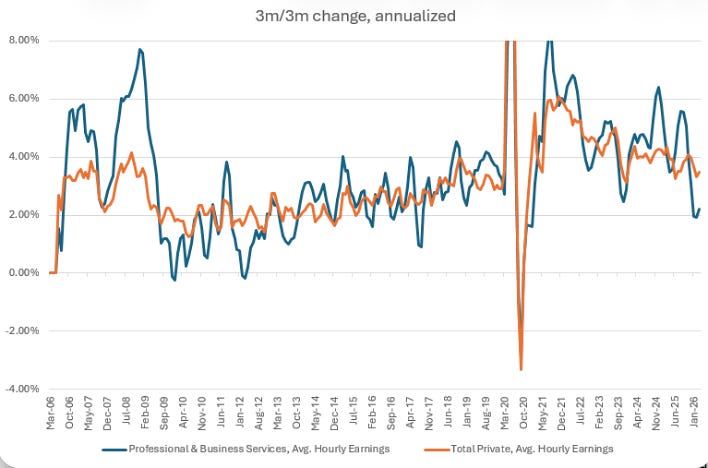

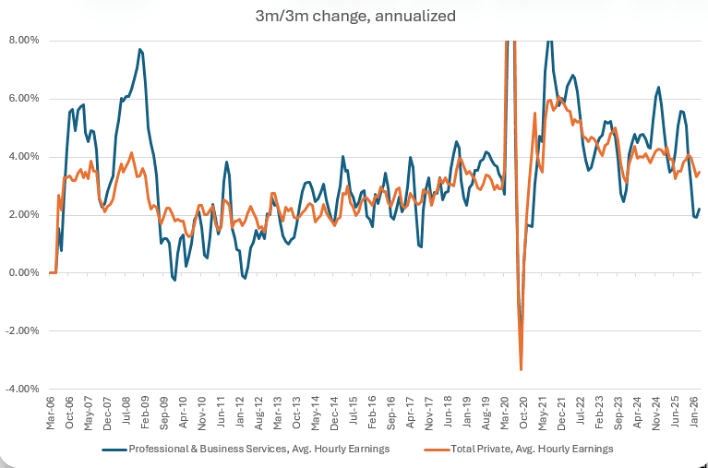

In terms of economics, workers in aggregate are accepting a lower rate of wage growth. In the US, wage growth has fallen to 3.5% from 6% a few years ago. While tying this directly to AI is difficult, the simplest explanation is that companies are doing more with less, so demand for labor is ebbing. Hiring rates are in the fourth percentile, even though unemployment is not rising. Pay for “professional services” jobs — essentially college-educated workers with spreadsheets — is slowing fast.

-

In terms of markets, while the S&P 500 is up on the year, there are sharp divergences inside the index between AI winners and losers. SanDisk is up 150% this year on AI demand, while Workday is down 40% because it is viewed as an AI loser. Ten-year Treasury interest rates have risen this year (prices down) due to the war. Within the bond, real yields have fallen due to expectations that higher oil prices will slow spending, while expected inflation has risen. This year the dollar is losing ground to the Chinese RMB, and US stocks are underperforming emerging-market stocks (+5% versus +15%).

-

In terms of politics, the recent war highlighted how fractured and chaotic global policy and power have become. I am still not clear what exactly the goal was. In addition to the belligerents, China, the EU, Pakistan, Japan, the GCC, and many other countries all had a significant say in the policy outcome.

-

The optimal portfolio this year so far has been long emerging markets (unhedged), short US ten-year bonds, and short the dollar. Put differently, the highest-expected-return portfolio looks quite different from what would have made sense in the past. Policy is indeed erratic. With no reliable US security guarantee, the scramble for AI mastery is now overlaid on a scramble for energy and defense autonomy.