Substack Library

GlossaryPrice Shock

March 6, 2026Not investment advice.

We are in the midst of a shift in market pricing and expectations driven by erratic policy that will continue until policy shifts.

I like short-term interest rates of central banks that are suddenly discounting tighter monetary policy, and stocks getting dislodged amid a panicked flight for cash, but doing so in a way that hedges my risk to an equity market meltdown.

In more detail:

-

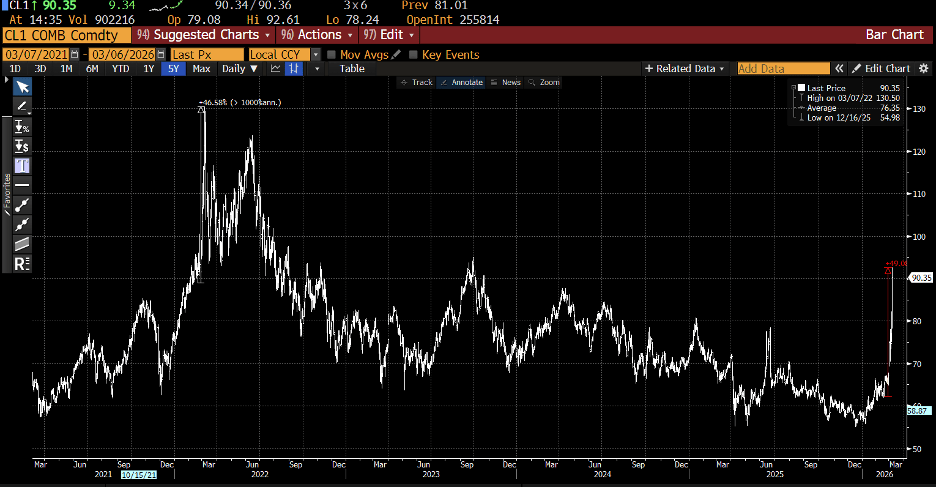

The energy shock of the US and Israel attacking Iran is roughly the same as the one where Russia invaded Ukraine. Crude prices rose 46% then and are up about 50% now. European gas prices are up 100%. The root cause is the same—reckless policy.

-

The 2022 energy price spike coincided with an inflation acceleration that led to substantial central bank tightening and a significant drawdown in equity markets. This episode is probably different because Putin is still fighting and the White House says this is not a forever war. But they also said they would not get involved in such wars in the first place, so to manage money I need to be prepared that the White House will not change course, even if the most likely case is that it does. I still don’t understand the goal and neither, perhaps, do many of the participants.

-

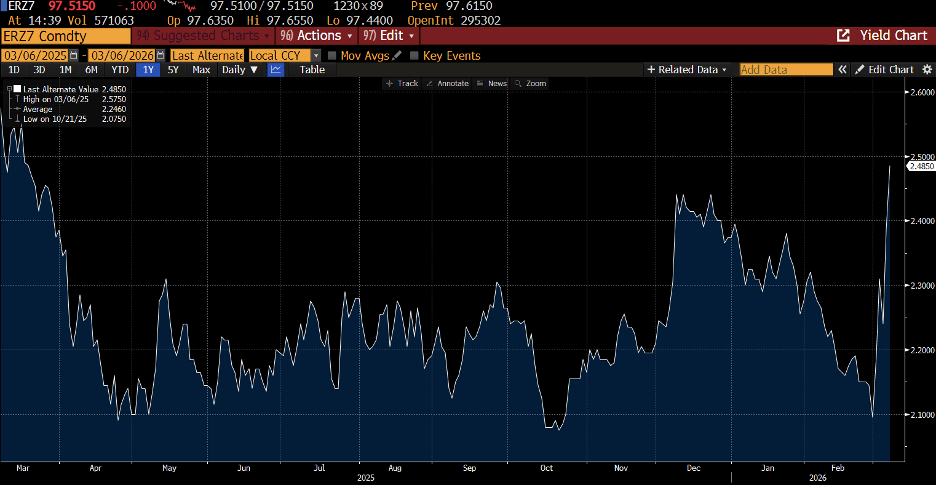

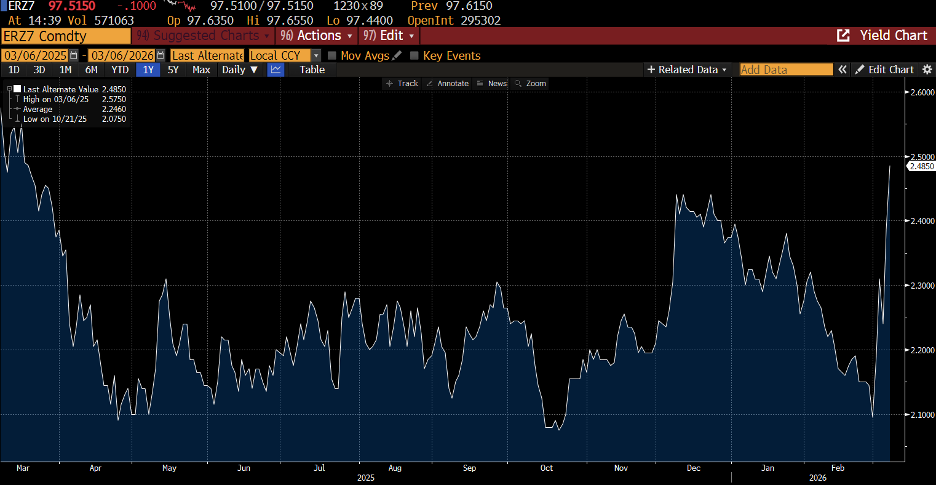

Markets price off of discounted conditions, constantly looking forward. In Europe, interest rate expectations have risen almost 50 bps in 5 days. That seems wrong. If I were the ECB, I’d do exactly nothing, not abruptly jack up rates. Moreover, European inflation is tame. In the US, labor market indicators are uneven but do not give the Fed ammunition to do much.

-

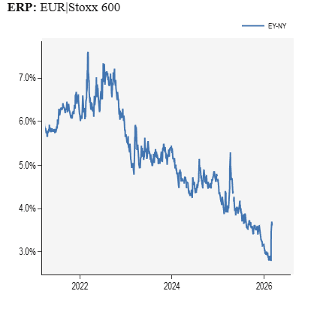

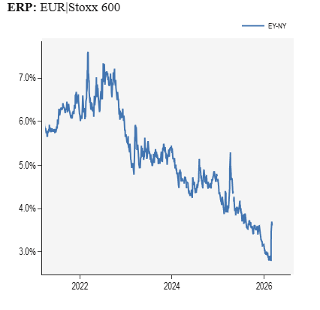

Equity indexes are a different matter. We track the “risk premium” in equity markets. Given the strong run of equities and the sell-off in bonds, the earnings yield—a rough proxy for the risk premium—for most major indexes is low. I show our measure of the risk premium in Europe below (to match with the bond yields above). The risk premium could rise quite a bit higher before being competitive with now-higher yields. The US and other major indexes look the same. When markets are stable, this does not matter much. When the wheels come off the bus, this matters.

-

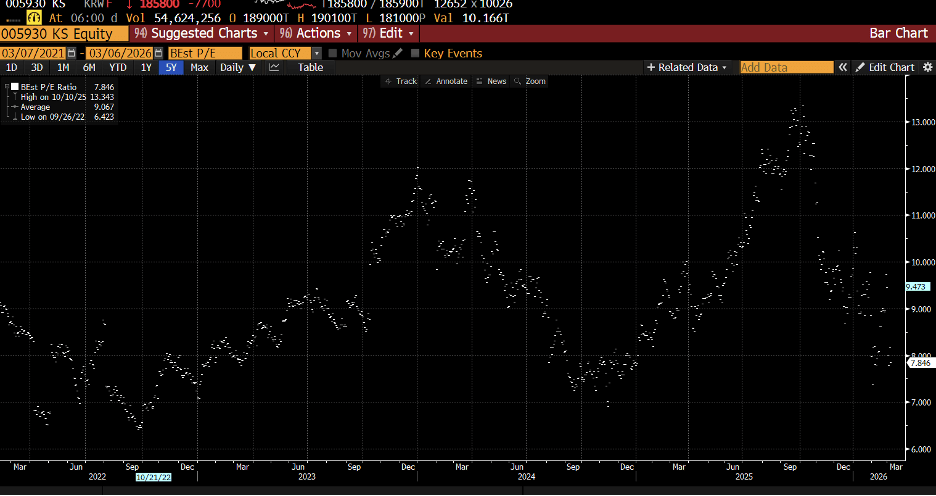

Individual stocks are priced differently. While I don’t have a position, it’s interesting that the forward PE of Samsung is now 7 after the Korea market crash this week.

-

Finally, the dollar rose this week as investors, particularly dollar-based ones, closed positions and moved to cash. US policy is now at least as, if not more, erratic than that in foreign countries, and this is leading both to Americans leaving the US and will, once the dollar squeeze ebbs, lead to a rise in foreign currencies. Yes, the US is home to leading-edge tech companies, but so are a number of countries, like Korea, and their policy is orderly.