Substack Library

GlossaryScholz, Xi and McCarthy’s Choice

April 10, 2022The more Buchas are revealed, the more stark the moral choices both government leaders and the rest of us face. It’s not overdramatic to say that the fate of liberal, open society hangs on what choices are made. The person who faces the most immediate and difficult choice is Germany’s Olaf Scholz. China’s Xi and House Republican Leader McCarthy also matter. Politicians, like us all, are motivated by self-interest. It’s also true that most ethical teaching, both Western and Eastern, remind us that harmony is only achieved by balancing our own interests against the legitimate interests of others.

Scholz’s Russia Energy Choice

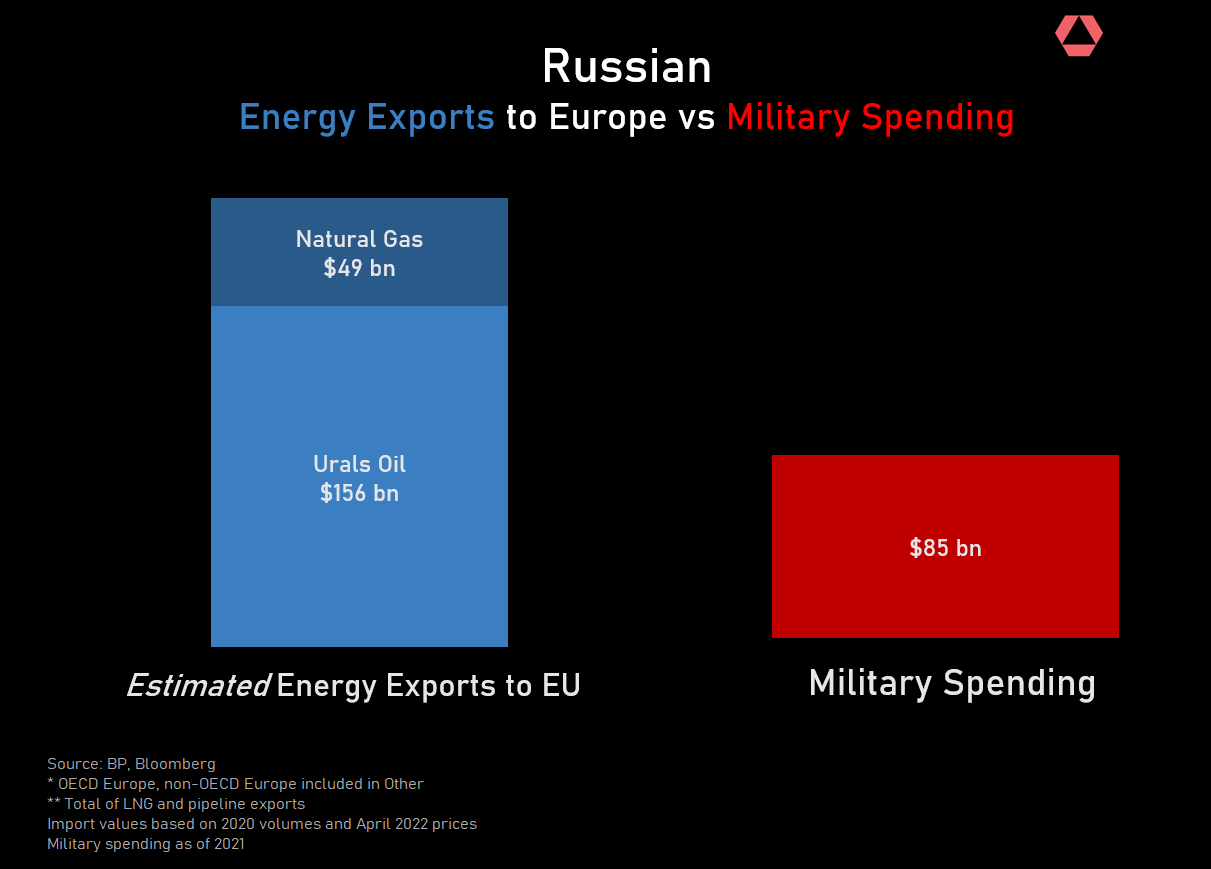

War is expensive. Russia relies on European energy consumption to pay for it. Below are the hard numbers. Before the ruble collapsed, the Russian economy was about $1.5 trillion.1 Military budgets are typically around 3% of GDP spending, give or take. Let’s assume in war time Russia’s military spending grows and that they pull money from other places, say Russia’s military spending is 5%+ of GDP, or $85 billion. (For context, the US spends around $750 billion on the military because the US economy is so much larger). Working with the brainiacs at Rose Technologies, we estimate Europe is currently paying Russia about $200 billion a year to heat their homes, drive cars and run factories, meaning that the most obvious, powerful lever the West holds to shut down what Ukraine’s Zelensky describes as genocide is cutting off this flow of money.

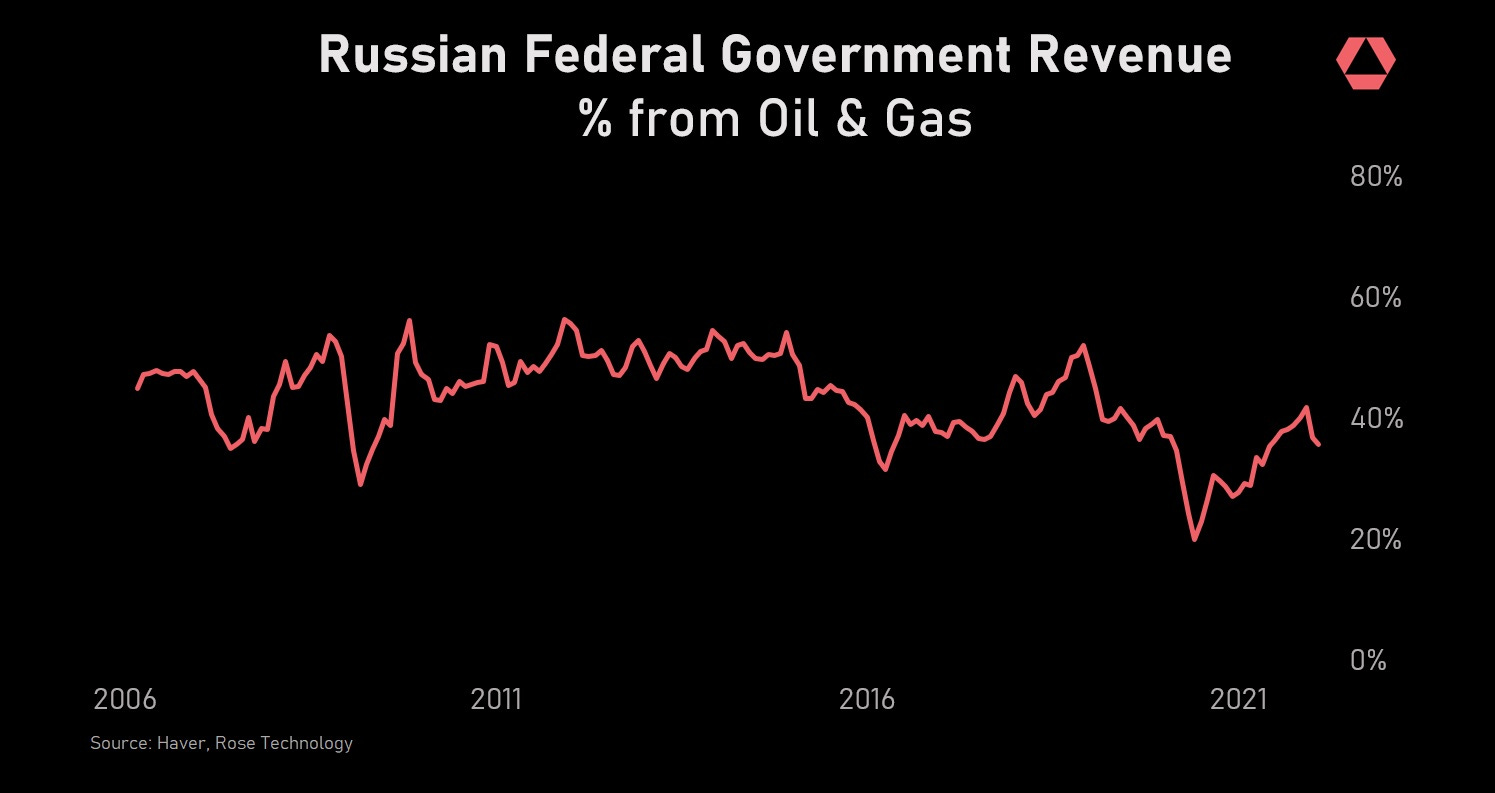

Cutting off this money would devastate Russia’s economy. Russia can borrow more money from its own citizens (war bonds) or re-direct other expenses (like pensions) but there are limits to what Russia can spend on weapons without selling energy to Europe. About 40% of total Russian government spending comes direct from oil and gas revenue as the chart shows.

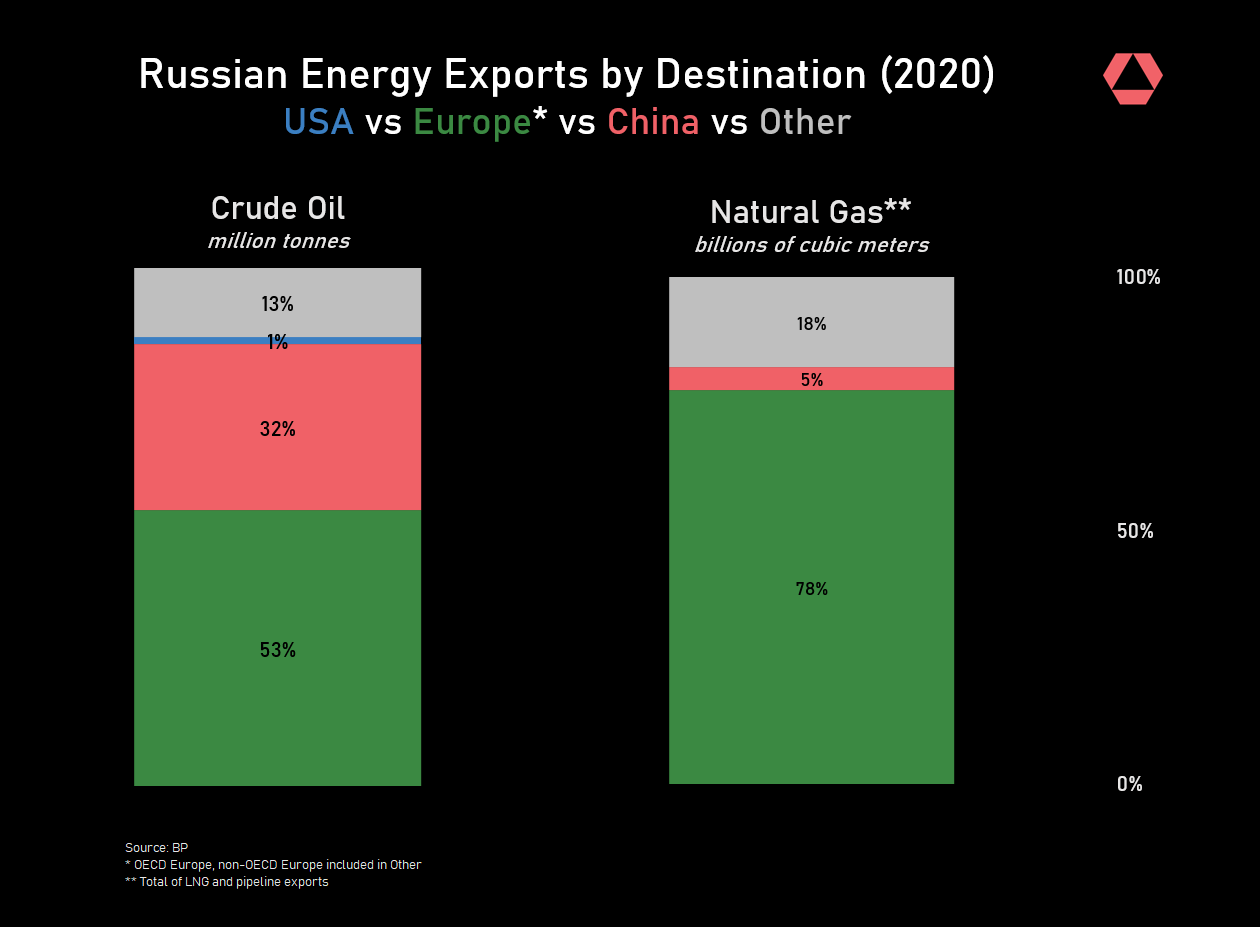

Yes, Russia exports energy globally. But If you look at the breakdown of this revenue, the vast majority of it goes to Europe.

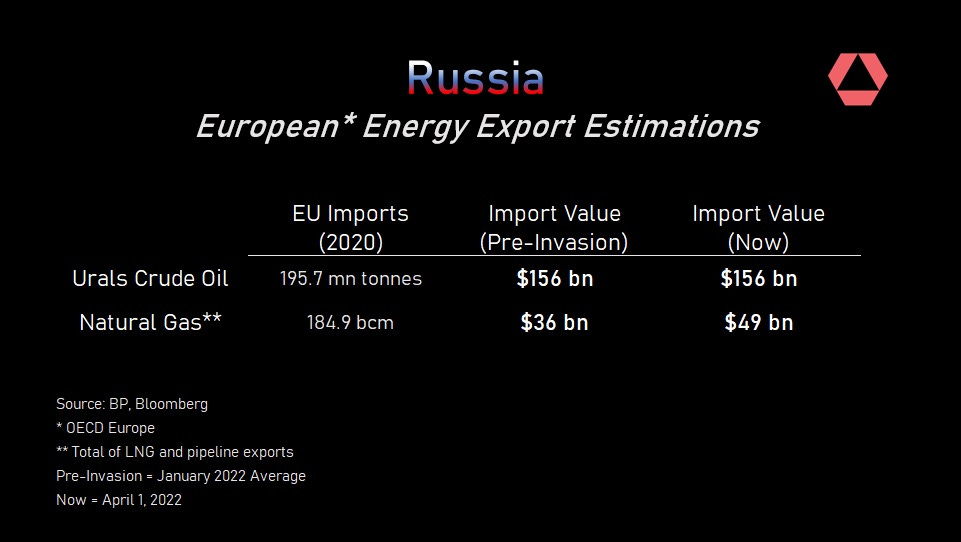

To calculate how much money Russia is earning, you need to look at both the volume of exports and the price. While the US and now Lithuania have said they will stop buying Russian energy, by and large Russia’s volumes are unchanged, which means that Russian revenue is up because prices have risen, as the table below shows, due to higher natural gas prices. For reference, the Kremlin earned about $60 billion in commodities revenue from Europe and the US in 2020, when prices were much lower.

Germany, Europe’s largest economy, has said that it wants to get off Russian energy in forty-eight months. However, Germany’s economic minister warned cutting off Russian gas sooner would inflict “more damage on us than them.”2 I guess it depends on how you measure “damage.” Clearly taking such a step is risky for Germany’s economy and its politicians. In France, Macron is being attacked by the right for raising French prices, when his policies have nothing to do with it. Le Pen is banking on voters not being clever enough to see that. How much cutting off Russian energy is in Germany and Europe’s self interest depends on how much people like Scholz weigh the legitimate interests of Ukrainians not to get murdered.

Xi’s Putin/Covid Choice

Xi’s choice is around telling the truth about what is going on in Ukraine and recognizing that domestic Chinese vaccines don’t work nearly as well as mRNA vaccines (more on Covid in the investment section). There is a new feature on Apple’s Safari that allows you to quickly translate any foreign press report. This allows you to read what Beijing is and most importantly isn’t saying in the news. There is very limited coverage of the war and the differences in vaccine effectiveness. You need to hunt for it, meaning Xi doesn’t want the Chinese to know the truth.

Instead, Party cadres are undergoing training about how effective Putin has been as a leader and there are lots of “whataboutism” editorials that argue NATO forced Putin to attack or the US has done terrible things. That the US shouldn’t have invaded Vietnam or Iraq2 says nothing about the moral merits of Putin’s invasion. Truth is truth.

China’s system mimics Russia’s. There are smart technocrats in both. The person who runs Russia’s Central Bank, Nabuillina, is a clean, smart technocrat. But these people, as I’ve noted before, don’t matter that much in a single person system.

This looming question is Xi’s decision on Taiwan. One might think that seeing what has happened to Putin would soften Xi’s enthusiasm. But I am not convinced. While no one can say for sure, if the press in China was given the green light to note how Ukraine is a flagrant violation of China’s cherished principle of non-interference, I’d feel better. Chinese then could see for themselves what the costs of invasion are. I see no sign of that.

McCarthy’s Truth Choice

McCarthy’s choice is around repeating a lie to retain and grow power. McCarthy is of course a Californian Republican and House Minority Leader. He is also representative of a number of Republicans who are refusing to participate in the January 6 investigation and perpetuating the big lie. Leaders like Liz Cheney (R. Wyoming) and Sen. Mitt Romney (R. Utah) are the courageous, valiant outliers. While everyone lies a little (“it’s great to see you!”), big lies, as we have seen with Putin, metastasize. As 2024 approaches, I am concerned about challenges to election integrity. Once you start telling crazy lies—like that Ukrainians and Russians are one people—where do you stop? America has pulled through so many difficult crises in the past, I’m hopeful it will again but also cognizant that, yes, indeed, sometimes countries fall apart.

Investment Implications

As I’ve said from the beginning of the year, this is a tricky environment. THIS IS NOT INVESTMENT ADVICE. I AM SHARING WITH YOU WHAT I AM DOING, FOR YOU TO TAKE OR LEAVE.

I am seeing: rising inflation, energy re-organization and great uncertainty.

-

Inflation. There is a big inflation problem caused by: pandemic stimulus, China’s COVID policy which is getting, by the way, much worse. Shanghai is in lock down and this is impacting Chinese ports, thus creating more supply chain tangles, which is inflationary. Plus, war in Russia, which is driving up prices of energy and agriculture. The Fed’s credibility is now on the line. They need to raise rates a lot and importantly need to get long-term interest rates up enough to slow demand for houses and cars, which will ripple through the whole economy. Forecasting where rates needs to go is less important than watching the reaction in the market. When stocks, houses and energy prices start to fall, that’s a sign the tightening is working. So far the expectation of tightening isn’t doing much. My conclusion: stay short bonds, particularly at the long end, cut banking stocks because now the risk of recession is rising, which often causes credit problems. Logically, I should be much shorter bonds but I’m worried about a weird fat tail event, like Russia using chemical weapons, that leads to a big counter-trend move.

-

A huge re-organization of global energy markets such that Europe stops using Russian energy and instead uses US natural gas. This is super bullish those companies who are tied into non-Russia energy infrastructure. Prices have risen, I think they rise more. That’s where a lot of my commodity exposure is.

-

Great uncertainty. I am uncomfortable. I’m a bit high strung to begin with but I am indeed nervous now given the risks cited here and in other posts. I’ve got about a 30% position in cash, which is huge for me. In the last year, I’ve watched a few very smart people loose a large percentage of their wealth, two of them wiped out completely. Another rule of mine is that I have enough risk on that I can sleep well and write books well. If that’s not happening, I increase my cash position.

-

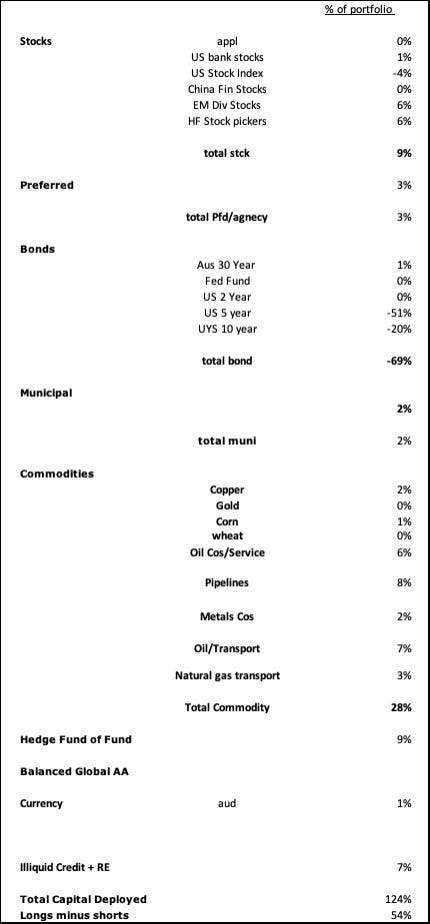

I’m up 1.7% for the year, unaudited and some of my illiquid returns have not yet reported and should help a bit. Below are my holdings.

These numbers are calculated in dollars, so they are easier to digest. Since the ruble has lost about 40% of its value since the invasion, the actual dollar numbers on all these calculations would be even worse.

https://www.reuters.com/world/europe/germany-moving-step-by-step-toward-russian-energy-embargo-habeck-2022-04-04/