Not investment advice.

It’s possible Warsh raises rates this summer or in September. This is not expected and not discounted, but if you wanted to make a power move as a new Fed governor—get inflation closer to target and also lean in the direction of others on the board—you might endorse such a move.

The Fed chair job is both technical (knowing which way the economy is going) and theatrical (commanding respect). To be good, you either need to be exceptional at one or pretty good at both. Of the Fed chiefs in my career, Bernanke was the most analytically sophisticated. He had written books on depressions and so was ideally placed in 2008. Greenspan and Volcker in particular had presence, and if Warsh wants to create such an impression, an early, proactive hike would be in Volcker’s spirit.

The economic situation is straightforward. Unemployment is low, the US is running a 5%+ budget deficit, and AI capex spending over the next 12 months will grow by around 30% to … $1 trillion, more or less. That is 3% of GDP. And that spending does not include the off-balance-sheet spending by the big AI spenders, which makes this number even larger (though some of this money leaks abroad to places like Taiwan that make the chips). So the US is running perhaps a 9% public/private stimulus.

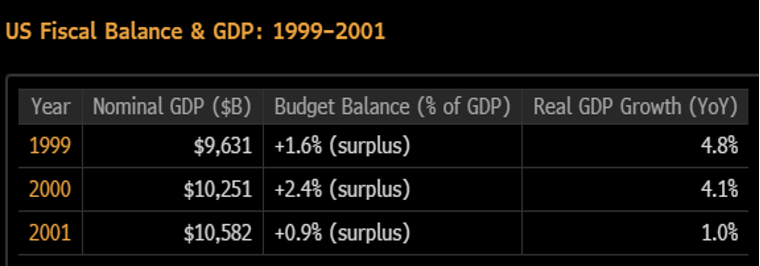

The difference between this boom and the 1999-2001 boom is stark. Unlike in 1999, this time the government also has its foot on the gas. During the last tech upswing in the stock market, the US budget deficit was … negative (the government was in surplus) as shown below.

“Persistently high prices are a burden for the American people, but the recent past need not be prologue,” Warsh said last week. The possibility that the Fed might tighten explains why currencies like the Swiss franc, which yields zero, have begun to weaken. Expectations of tighter US policy, rising real interest rates, and hot IPOs are drawing in capital.

It will be hard to get the economy to slow unless the stock market goes down, and the stock market won’t go down until households stop buying or earnings, which are strong, weaken. In 1999, when the Fed first raised interest rates during a tech stock frenzy, stocks initially fell 12%. However, they subsequently rose 110%.

Warsh wants to do what Powell wouldn’t—get inflation down. I expect higher short-term bond yields, a stronger dollar, a stock market wobble that then vaults higher.

(Note to readers—this is my post for the week. No post Friday.)

This document is strictly confidential and is intended for authorized recipients of “A Letter from Paul” (the “Letter”) only. It includes personal opinions that are current as of the date of this Letter and does not represent the official positions of Kate Capital LLC (“Kate Capital”). This letter is presented for discussion purposes only and is not intended as investment advice, an offer, or solicitation with respect to the purchase or sale of any security. Any unauthorized copying, disclosure, or distribution of the material in this presentation is strictly forbidden without the express written consent of Paul Podolsky or Kate Capital LLC.

If an investment idea is discussed in the Letter, there is no guarantee that the investment objective will be achieved. Past performance is not indicative of future results, which may vary. Actual results may differ materially from those expressed or implied. Unless otherwise noted, the valuation of the specific investment opportunity contained within this presentation is based upon information and data available as of the date these materials were prepared.

An investment with Kate Capital is speculative and involves significant risks, including the potential loss of all or a substantial portion of invested capital, the potential use of leverage, and the lack of liquidity of an investment. Recipients should not assume that securities or any companies identified in this presentation, or otherwise related to the information in this presentation, are, have been or will be, investments held by accounts managed by Kate Capital or that investments in any such securities have been or will be profitable. Please refer to the Private Placement Memorandum, and Kate Capital’s Form ADV, available at www.advisorinfo.sec.gov, for important information about an investment with Kate Capital.

Any companies identified herein in which Kate Capital is invested do not represent all of the investments made or recommended for any account managed by Kate Capital. Certain information presented herein has been supplied by third parties, including management or agents of the underlying portfolio company. While Kate Capital believes such information to be accurate, it has relied upon such third parties to provide accurate information and has not independently verified such information.

The graphs, charts, and other visual aids are provided for informational purposes only. None of these graphs, charts, or visual aids can of themselves be used to make investment decisions. No representation is made that these will assist any person in making investment decisions and no graph, chart or other visual aid can capture all factors and variables required in making such decisions.