Substack Library

GlossaryThe Clock Is Ticking

March 26, 2026Not investment advice.

If a deal is not agreed to soon, there will be a Covid/2008-style abrupt slowing in growth as oil-derived products go into acute deficit. In more detail:

-

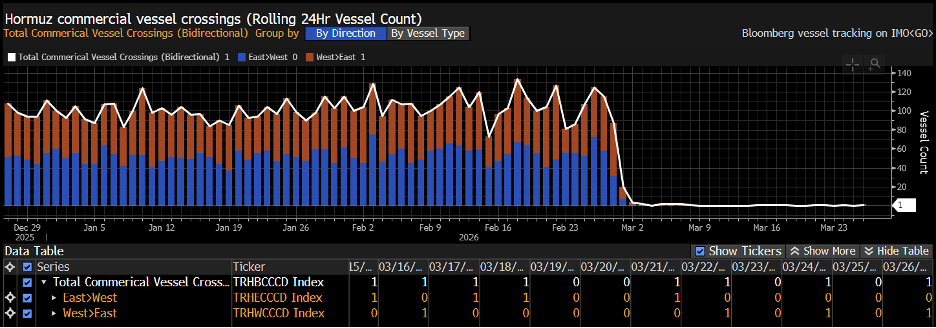

The US and Israeli attack on Iran did not envisage the Strait of Hormuz (SOH) being closed. It is now mostly closed. Below is the ship traffic, though there is a slight up-tick more recently not shown in the data below.

-

Asia gets most of its oil via the SOH. The crude mostly goes to India and China, who refine it into products that Asia consumes. There are now acute shortages of these refined products. Asian airports will run out of jet fuel in the near future if the SOH remains closed. That’s the part of this that is like Covid. There will be acute, abrupt cessations of activity, empty roads. In the poorest countries, those most dependent on energy imports, this is already underway. Pakistan has closed schools to reduce oil consumption. The Philippines has implemented a four-day work week. Airlines are cutting back routes.

-

Once the shortage becomes acute in one part of the world, it will spread. From jet fuel, it will move to diesel in Europe. The Americas are less impacted because the US, Canada, Brazil, Argentina, and others all have domestic oil production.

-

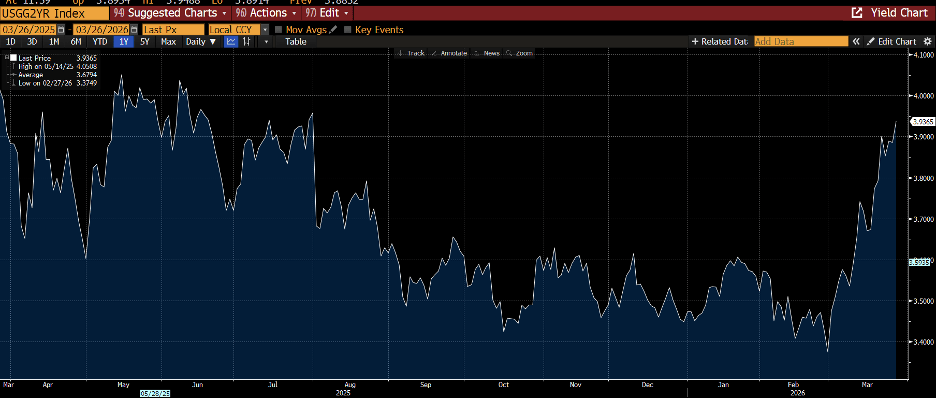

There has been an abrupt tightening of financial conditions. Oil is obviously higher, but interest rates (shown below) are too. These shifts are rapidly removing money from the economy that would otherwise be spent and is daily increasing the risk to stock markets. If nothing changes, growth will begin to contract.

-

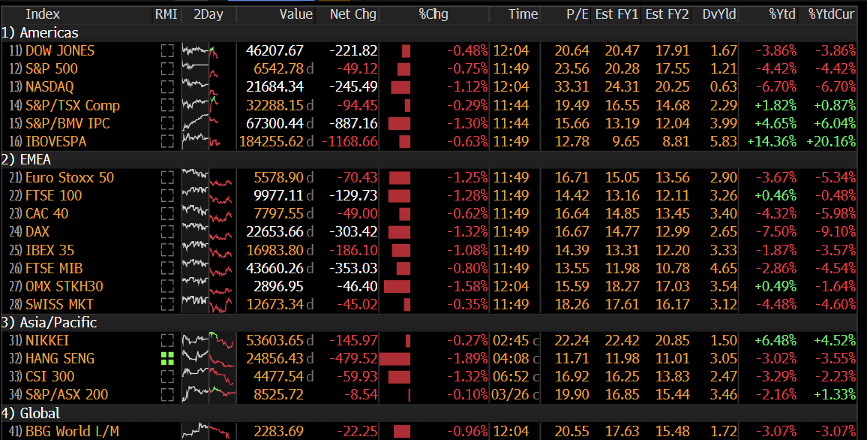

Stock markets are holding in there because of a belief that a US Iran deal is imminent. Many remember the violent stock market reversals in April. It’s true that the closer the global economy is to a precipice, the more pressure there is on Trump to pay the Iranians whatever they want (sanctions relief) to open the SOH. But it’s plausible that Iran waits for as long as they can, making the fuel shortages more acute.

-

Each time financial markets have been closer to the precipice, like Monday morning, the White House verbally intervenes to say a deal is close. This is policy makers trying to delay a market panic. In March 2020, President Trump also said the Covid virus is “going to disappear, it’s like a miracle, it will disappear” and the comments about an imminent deal have that flavor.

-

I can’t predict how the Iranians will respond to US entreaties. What I can say is that if they delay we are going to see an acute, undiscounted decline in growth that is bearish stocks and bullish short-term interest rates.