Substack Library

GlossaryThe Next Shift

July 10, 2026Not investment advice.

Each year can be divided into a few regimes or shifts. The first two months of the year were marked by concern the Fed would lose independence and the AI trade was dead. US stocks ground lower, while foreign stocks and gold rose. March until recently was dominated by the war. If the US wanted to win, they’d have to put boots on the ground, which would have sent oil prices much higher. But the White House didn’t want to bear the cost, so it retreated and oil prices fell. The last part of the year may be about an adjustment in US monetary policy, a dollar bull market, and confirmation that investing in AI is indeed profitable.

In more detail:

-

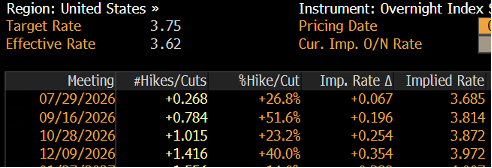

The market puts low odds (26%) on the Fed hiking rates this month and roughly 50/50 odds on a hike in September. Against those probabilities, the reality is:

a) the US economy is growing fast

b) new leadership is an opportunity to reset inflation expectations

c) an early hike reduces the need to hike more later

d) inflation is above target

e) the stock market is at highs

f) a hike may lower long-term interest rates, helping housing

g) given that the market is already discounting some hiking, if the Fed doesn’t hike, its hawkish credentials could erode

h) a lot of other Fed members are calling for hikes, so building consensus is possible.

-

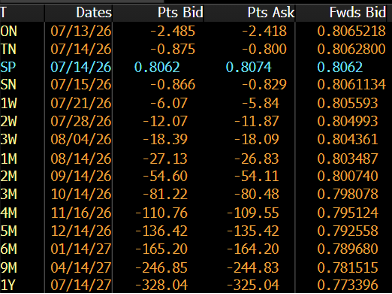

A tighter Fed is bullish for the dollar. For example, the Swiss Franc is priced to appreciate 3.7% versus the dollar despite flat Swiss growth, inflation below target, no connection to AI, and a central bank that is threatening to intervene if the currency strengthens against the USD—which has a strong economy and a central bank that may tighten, as noted above.

-

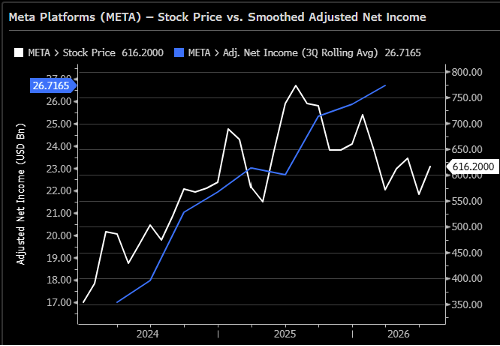

Mega-cap tech has underperformed this year, meaning these stocks are now priced for slowing earnings growth even as:

a) earnings are accelerating

b) the Magnificent 7, like Meta, are investing in technology that should be transformative for their moats

c) they are monopolies or pseudo-monopolies. Beyond Google, what ad firm can harvest the personal data of 4 billion people and bombard them via novel algorithms?

-

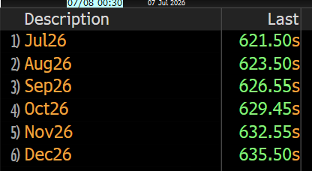

None of this is certain, so I look for hedges. Sometimes the best hedges are across assets. Copper prices are discounted to rise 2% before the end of the year despite:

a) surplus supply in the US

b) weak Chinese growth

c) lack of fresh US tariffs on copper

d) data centers shifting away from copper and toward fiber, which provides faster speeds.

The most likely path is modest Fed tightening, higher stocks, a stronger dollar, and a flatter curve. But there are tail risks, and I like copper as a hedge in the downside tail.