Substack Library

GlossaryThe Practice

May 3, 2024You have to choose, do you want to be number 1 or do you want to be happy?

Thich Nhat Hahn

THIS IS NOT INVESTMENT ADVICE. INVESTING IS RISKY AND OFTEN PAINFUL. DO YOUR OWN RESEARCH.

The Practice

If markets were easy, they would not lead to waves of anxiety in the darkest hours of the night or aching back pain the next morning. Your body keeps the score and part of managing money is managing pain. Given this, you need a discipline to keep your wits about you.

The specific practice is specific to the individual investor. Warren Buffet is always long stocks. That works great – if you are in the US and it isn’t the 1930s. If those two conditions are not met, you are in for a rough ride. My own approach is specific to my training and background, including watching an empire (the Soviet one) implode early in my career, and later spending decades on trading floors and inside the biggest hedge fund in the world, Bridgewater. Also, like many of you, I’ve seen my share of difficult things, as I described in Raising a Thief. That’s made me aware (overly aware?) of how things can go awry.

If you play a sport or practice a religion, you know the importance of practice. I row competitively, so I’ll use that as an example. You can’t do well in races if you don’t a) get in a certain number of miles on the water b) spend part of those meters on balance and technique c) lift weights d) sleep and e) keep your weight down. If you are doing those things, you will not win but you will be going about as well as you can go. At that point, what happens depends on the competition.

In macro investing, there is also a practice. The practice is stepping back to absorb the big picture and then zooming into the detail and then, once again, zooming back out. This means doing two things.

First, scanning the world along the schedule of what I show below.

Second, tying these observations to frameworks you evolve over time. For instance, when I started out, I never bought stocks that were “expensive.” Now, sometimes I do.

You must have anchor points. One of mine has been that developed world economies only grow so fast. If cash rates are 5% and the potential growth of the economy is around 1% or 2%, the economy will slow. Whether this happens fast or slow, it will happen and I have been adjusting my positions around that expectation.

In these posts, I am moving around the matrix above and then tying it to frameworks and sometimes evolving those frameworks. That’s it. I do it because it works. For me. And because I want to share it with you.

Japan

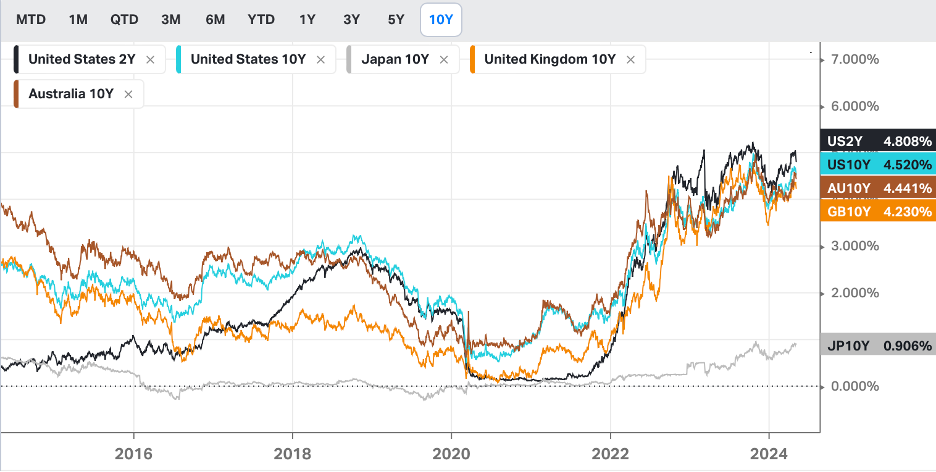

When I look at the world this way, I notice things. Like that most places in the world have the tightest monetary policy and highest bond yields they’ve had in years. Except for one place: Japan.

The interest rate on cash in Japan is zero and inflation is around 2.5%. That means the real (inflation-adjusted) price of cash is negative 2.5%. In the US and Europe, that number is +2.5%. Recall the “anchor” that I mentioned above. 5.5% cash rates (US) with 2.5% inflation is tight. 0% cash rates with 2.5% inflation (Japan) is loose.

Those differences drive capital from one area to another, like a magnetic force, which is why the yen is collapsing.