Substack Library

GlossaryThe Wheels Come Off the Bus

March 12, 2026Not investment advice.

There are two big pressures in global markets, pushing in opposite directions.

The AI boom is a productivity shock that is good for profits, reduces inflation, and spreads wealth around the world. That’s the trade many had on.

The war in the Middle East is a negative productivity shock that boosts inflation and lowers growth. Many had hedges on for this risk, but these hedges were small in proportion to the primary risk.

The first force was supposed to be the dominant one and the second force an intermission. It isn’t working out that way, forcing the sale of billions of dollars of assets.

The war lacks clear goals and involves 18 countries—not including reports that both Russia and China may be involved. The market is pricing in a rise in energy prices, monetary tightening, and falling profits. So far stocks are down a few percent, but they will be down a lot more if energy doesn’t start flowing soon—and, from what I can tell, it won’t. Perhaps many investors were whipsawed last April following Liberation Day and are reluctant to do the logical thing now, which is to buy more oil and sell stocks.

In more detail:

-

Iran mounted a more chaos-causing defense than anticipated. While Western military experts assert the war is going well; from the seat of an investor, the same regime remains in place and oil, natural gas, and other prices are substantially higher than before the attack. In literal terms, the money you would have spent on going out to dinner instead goes to filling up a car with gas.

-

Many of the assets that were supposed to hedge such a risk—gold, bonds—have added to risk. The only trades that have worked are long oil and short stocks. The risk of a significant stock market decline has increased. Higher energy prices and interest rates are colliding with high valuations. Short-term interest rates are up 30 to 50 basis points in 11 days.

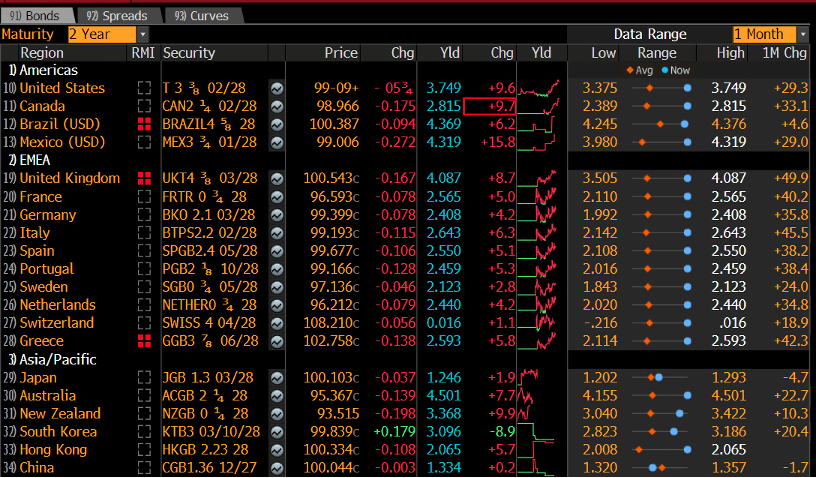

This market is now pricing in rate hikes in many parts of the world. The bond market is ignoring the coming growth shock and focusing on inflation, which might be because 2022 is fresh in people’s minds and central banks might indeed raise rates if energy prices don’t rapidly fall.

A return to more normal P/Es, which higher interest rates will induce, would suggest a 20% decline in stock prices. If stock prices fall, discretionary spending will grind to a halt. P/Es have not mattered for a few years, but they might now.

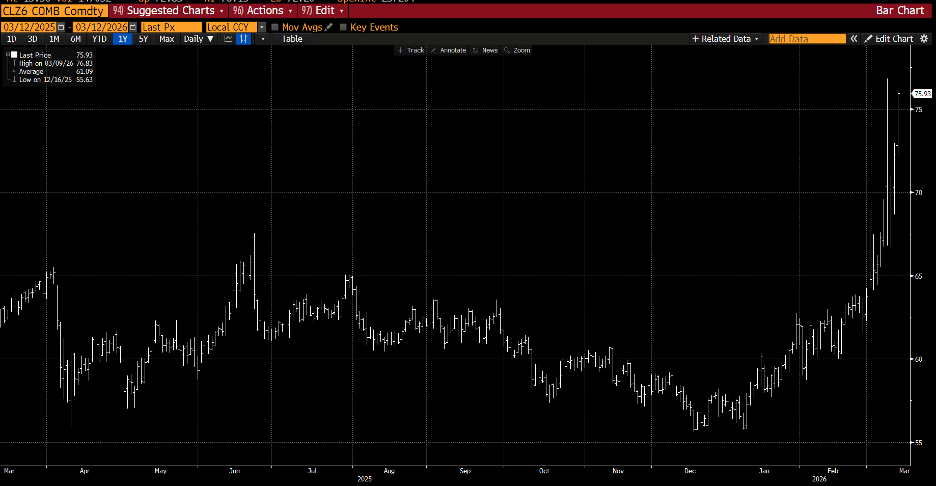

The consensus is that Trump will de-escalate and that, after a few days, so will Iran. Longer-dated oil contracts are now hitting new highs, however; traders are pricing in a freezing of traffic in the Strait of Hormuz.

Once the Strait closed, prices rose. Then producers stop exporting and storage begins to fill up. Once that storage fills up, they shut the pumps, which then causes another rise in prices. We have yet to see that second rise in prices, but it could come any day now.

-

This is happening amid jitters in the credit market and a gating of fund withdrawals by more institutions. Essentially, there is a bank run on illiquid credit. By our calculations, the actual amount of bad debt is small, but the gating adds to market stress.

-

The build-out of AI data centers continues but is dependent on cheap energy. So the second trade (oil shock) begins to impinge on the first force (productivity shock).

-

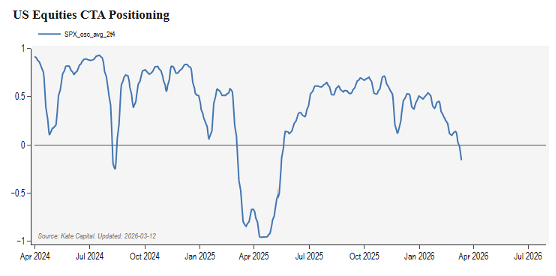

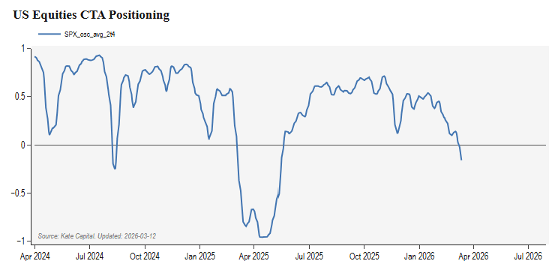

Selling of stocks begets selling. Trend-following investors are now turning negative, which will create even more algorithmic selling.

-

The market is no longer responding to Trump’s tweets the way they once did. On Monday when he said the war was almost over, stocks reversed. He repeated this later in the week, but traders could see oil prices picking up and sold stocks. It looks like the market is losing confidence in leadership.

Maybe this ends soon, but one needs to have a plan if that is not true—and that plan needs to include the possibility that stocks fall substantially.