Substack Library

GlossaryWars, Tightening, AI

July 17, 2026Not investment advice.

Now, it’s clear that you in the West, living hypocritically, think that power, vigor, force, are a bit archaic. You believe in rules, with your lawyers communicating by certified mail and earning million-dollar fees.

Giuliano Da Empoli, The Wizard of the Kremlin, 2022

There are three forces buffeting markets—wars, tightening, and AI.

Wars

Oil is up about 20%+ in the last 10 days. The US is attacking Iranian infrastructure, Iran is firing cruise missiles at boats and GCC countries, and the Houthis have attacked targets in the Red Sea.

Crack spreads are up 60%. This is the spread a refinery earns by turning oil into gasoline or diesel. The squeeze is less in oil prices and more in refined products. Not only is capacity offline in the Middle East, it is almost entirely offline in Russia. Today, Ukraine hit a refinery deep in Russia.

Equity investors I speak to are uninterested. I attribute this to Trump retreating on tariffs and Iran when markets became unglued, along with a tacit assumption that the same will be true now—if this gets ugly, it will stop.

Yet, a shift in energy prices mechanically shifts cash flows. Energy exporters like Canada or Norway receive cash, while energy importers like Japan and China disgorge it. The same is true with companies, some produce energy, all consume it. Moreover, assets that were in supply surplus, like copper, can go into potential deficit because key ingredients required for copper extraction travel via the Strait of Hormuz. Weak economies with falling inflation can turn into weaker economies with rising inflation. The key point—once you put war back into the mix, it shifts the flow of money and asset pricing. It may or may not be the dominant pressure, but it is undeniably a pressure.

Tightening

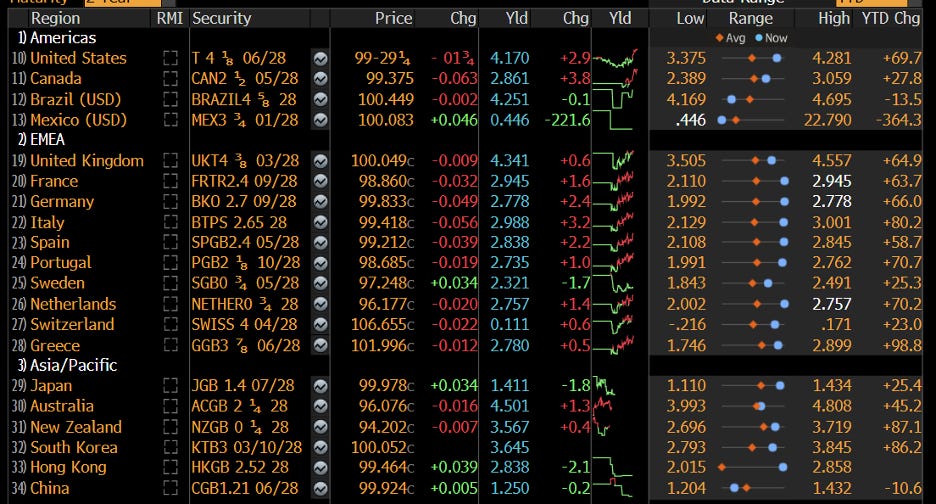

Over the last 7 months, a balanced mix of assets has gone sideways. Stocks went up, bonds went down. Said differently, risk premiums are gradually rising. Central banks in Korea, Japan, Australia, New Zealand, and Europe have all raised rates. The Fed has not yet, but may well be forced to if inflation doesn’t fall. Despite the volatility in oil, US nominal growth is still around 5% or 6%, and unemployment is low. Whether or not a central bank (the Fed) tightens is less important than the pricing. As the table below shows, two-year bond yields are up by half a percent to a percent this year, depending on the country. This is mostly driven by the wars. This week US data was unexpectedly soft, but war and AI spending is inflationary. If two-year yields move higher, stocks move lower or maybe go sideways.

AI

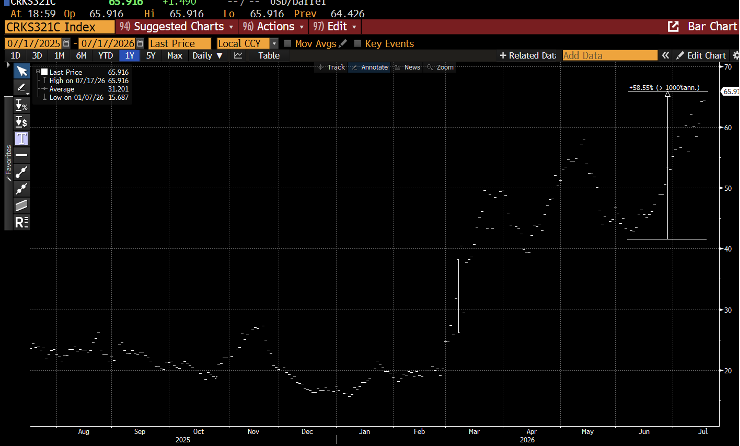

The challenge with AI is the known knowns and known unknowns. The known known is that many are long. The fundamental story is good. The leading companies are profitable. When I say many are long, I mean not only hedge funds but also households trading one-day options that boost volatility. This means that even if the story is good, stocks can correct easily—as they have now—because positions are widely held and sometimes levered. Small changes cascade. The chart below shows the NASDAQ. In the march upward, it has corrected multiple times. There is always a “reason”—sometimes it is tariffs (2025), sometimes war (March), sometimes weird changes in Japanese monetary policy (2024)—but the key ingredient in all of them is market structure and crowding. Where are we now in that process? Well, it depends a bit on war and tightening, but I suspect the market is still crowded, though far less crowded than it was a month ago. The known unknown is how big the TAM, or total addressable market, really is for AI. Does the spending on AI calm in two years or ten? No one knows. We figure it out quarter to quarter, and different assumptions yield very different conclusions. As far as I can tell, as I’ve said, the Mag 7’s future profitability is underpriced. That’s not how it has traded, however. It trades like these companies are spending money in ways that won’t lead to higher profits down the road.

It’s also true that if the stock market doesn’t hold these levels and falls another 5% or 10%, economic growth in the US will grind to a halt and the Fed will for sure not tighten. So these themes—wars, tightening, and AI—are independent yet inter-dependent.